If you’re looking to refinance—or in some cases buy a new home—a 10-year mortgage might be a good option for you. Here are the current 10-year mortgage rates and how you can find the right lender.

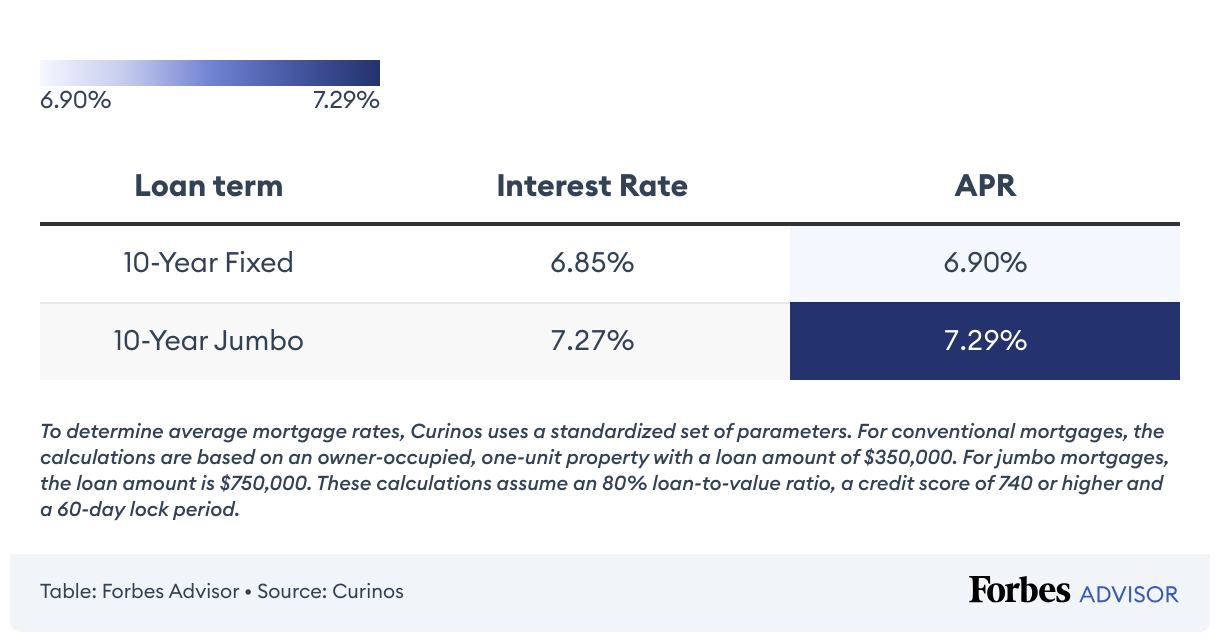

What Are the Current 10-Year Mortgage Rates?

How To Get the Best 10-Year Mortgage Rates

Studies have shown that borrowers who comparison shop get better rates than those who borrow from the first lender they find. The best mortgage lenders with the best rates are typically reserved for those with good to excellent credit.

If your credit profile isn’t strong enough for you to get the best mortgage rate possible, review your report and make any necessary changes to improve your credit. To qualify for the lowest interest rate possible, you’ll want it to be as strong as possible.

What Is a 10-Year Mortgage?

A 10-year mortgage is a home loan that lets you repay your lender over just 10 years. It could be a good option for you if you’re looking to refinance or if you want a speedy repayment period. Because the repayment period is so short—most Americans opt for 30-year mortgages—you’ll save considerably on interest payments. You’ll also build equity more quickly.

Even though interest rates are generally lower for shorter terms (like 10 years), you’ll still have higher monthly payments than you would with a 30-year mortgage—or even a 15- or 20-year.

How To Apply for a 10-Year Mortgage

If you’re considering refinancing your mortgage, you may want to start by contacting your current lender to see if they can offer you better terms. But it usually pays to shop around. You can get a mortgage through banks, credit unions and many online lenders. Compare rates with multiple lenders as well as the total cost of the loan, including fees.

On the other hand, if you’re considering a 10-year mortgage to help you purchase a home, make sure the monthly payments aren’t too high. Even though it may sound appealing to own your home free and clear in just 10 years, a lot can happen over that time period. A 15-year mortgage may be a safer compromise.

Related: How To Get A Mortgage: 7 Steps To Success

How To Pay Off a Mortgage in 10 Years

You can get a 10-year mortgage from just about any lender. But you might consider sticking with a longer-duration mortgage and paying extra each month instead. This is because the monthly payment on a 10-year mortgage will be significantly higher than one for a 30- or 15-year fixed-rate mortgage. If you have any financial problems down the road—unexpected medical bills, job loss—the flexibility to pay a little less each month will help.

There are a few strategies that will help you pay off your mortgage early. You can pay more toward your mortgage principal with every payment you make, opt to make bi-weekly mortgage payments or make lump sum payments whenever you have the means.

Pros and Cons of 10-Year Fixed Mortgages

While 10-year fixed mortgages can be a good choice for some borrowers, they aren’t right for everyone. Here are some pros and cons to consider when deciding if a 10-year fixed mortgage will work best for your needs:

Pros of a 10-year Fixed Mortgage

- Lower rates. Mortgages with 10-year terms typically offer some of the lowest interest rates available to homeowners. Loans with longer terms—such as 15- and 30-year mortgages—generally have higher rates. This can help you save a substantial amount of money on interest over the life of the loan. If you already have a mortgage with a longer term, refinancing to a shorter 10-year term could also be an option to reduce your overall interest costs.

- Shorter repayment. Paying off your mortgage in just 10 years means owning your home free and clear much sooner compared to a longer repayment period.

- Build equity. Home equity is the difference between the value of your home and what you still owe on your mortgage. Paying down your principal balance more quickly with a 10-year term will help you build equity in your home faster, which will make it available to you if you want to tap into it with a home equity loan or home equity line of credit (HELOC)—or if you’d like to make a profit by selling your home.

Cons of a 10-year Fixed Mortgage

- Higher monthly payments. Since your repayment term is shorter with a 10-year term, your monthly payments will be higher compared to what you’d pay with a 15- or 30-year loan.

- More stringent requirements. Since a shorter loan term will come with higher monthly payments, lenders will likely require you to have a higher income to show you can afford repayment. They might also expect you to have a higher credit score or meet other stringent eligibility criteria.

- Harder to find. Mortgages with 10-year terms aren’t always as readily available as some of the more popular loan options.

Faster, easier mortgage lending

Check your rates today with Better Mortgage.

Alternatives To a 10-year Mortgage

If a conventional 10-year mortgage doesn’t seem right for your situation, other options to consider include:

Conventional 15- or 30-Year Mortgage

If you’d prefer lower monthly payments, opting for a conventional loan with a longer term, such as 15 or 30 years, could be a good choice. Just keep in mind that these loans generally come with higher interest rates compared to 10-year mortgages, which means you’ll pay more in interest over time.

Government-Backed Loan

You could also consider a loan backed by the Federal Housing Administration (FHA), U.S. Department of Agriculture (USDA) or Department of Veterans Affairs (VA).

FHA and USDA loans are generally geared toward borrowers with lower incomes and poorer credit scores as well as first-time homebuyers. VA loans, on the other hand, are meant for active and veteran service members and their surviving spouses. These loans also require little to no down payment, depending on the program.

While government-backed loans can come with shorter terms, you also have the option to choose a longer, more affordable term if you’d prefer.

Frequently Asked Questions (FAQs)

Is a 10-year mortgage right for me?

A 10-year mortgage might be the right choice for you if you’ve already paid down a lot of your mortgage and are looking to accelerate your payments. It could also be a good option if you’re making an initial purchase and have the means to pay aggressively toward your principal while saving on interest costs.

Use a mortgage calculator to help you run the numbers and make an educated decision.

What is a good 10-year mortgage rate?

As of October 27, 2022, the average national annual percentage rate (APR) for a 10-year, fixed-rate mortgage was 6.71%—higher than the average 6.28% APR for 15-year loans but lower than the average 7.32% APR for 30-year loans. A good rate will be the lowest you can find with a lender you like and trust as well as minimal fees.

Keep in mind that your rate will depend on several factors, including your credit score and your down payment amount.

Are 10-year mortgage rates lower than 15-year mortgage rates?

Lenders typically offer lower rates on loans with shorter terms, so 10-year mortgage rates tend to be lower than what you’d get on a 15-year loan. However, rates vary depending on the lender as well as your credit score and other qualifications.

To find the best deal, be sure to shop around and compare your options with as many mortgage lenders as possible. It’s also a good idea to:

- Check your credit. Lenders will review your credit to determine your creditworthiness along with your interest rate. Checking your credit ahead of time can help you get an idea of where you stand.

- Use a calculator. You can use our 10-year mortgage calculator to see if you can afford the monthly payments.