- Kaiser Permanente – Best Overall

- Blue Cross Blue Shield – Best Provider Network

- UnitedHealthcare – Best for Breadth of Insurance Options

Les Masterson is a deputy editor and insurance analyst at Forbes Advisor. He has been a journalist, reporter, editor and content creator for more than 25 years. He has covered insurance for a decade, including auto, home, life and health. Before covering insurance, Les was a news editor and reporter for Patch and Community Newspaper Company and also covered health care, mortgages, credit cards and personal loans for multiple websites.

Les Masterson

Les Masterson is a deputy editor and insurance analyst at Forbes Advisor. He has been a journalist, reporter, editor and content creator for more than 25 years. He has covered insurance for a decade, including auto, home, life and health. Before covering insurance, Les was a news editor and reporter for Patch and Community Newspaper Company and also covered health care, mortgages, credit cards and personal loans for multiple websites.

Michelle is a lead editor at Forbes Advisor. She has been a journalist for over 35 years, writing about insurance for consumers for the last decade. Prior to covering insurance, Michelle was a lifestyle reporter at the New York Daily News, a magazine editor covering consumer technology, a foreign correspondent for Time and various newswires and local newspaper reporter.

Fact Checked

Michelle Megna

Michelle is a lead editor at Forbes Advisor. She has been a journalist for over 35 years, writing about insurance for consumers for the last decade. Prior to covering insurance, Michelle was a lifestyle reporter at the New York Daily News, a magazine editor covering consumer technology, a foreign correspondent for Time and various newswires and local newspaper reporter.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

Providing health insurance can help a small business attract—and keep—employees. One way small businesses can buy health coverage is through the Affordable Care Act (ACA).

We evaluated large insurance providers that offer ACA marketplace plans to find the best health insurance companies across the country. Kaiser Permanente and Blue Cross Blue Shield scored the best in our analysis.

Read more

Show Summary

- Best Health Insurance Companies for Small Business Owners

- Summary: Best Health Insurance for Small Business Owners

- How Does Small Business Health Insurance Work?

- Do Small Businesses Have to Provide Health Insurance?

- Small Business Health Insurance Options

- Small Business Health Insurance Requirements

- How Much Does Health Insurance for Small Business Cost?

- How To Get Health Insurance for a Small Business

- How to Compare Small Business Health Insurance Plans

- Methodology

- Small Business Health Insurance Frequently Asked Questions

- Next Up in Health Insurance

Best Health Insurance Companies for Small Business Owners

Summary: Best Health Insurance for Small Business Owners

Kaiser Permanente and Blue Cross Blue Shield are the best health insurance companies for small business owners, based on Forbes Advisor’s analysis. UnitedHealthcare also received high marks.

| Company | Forbes Advisor Rating | Plans offered to small businesses | Size of provider network | LEARN MORE | ||||

|---|---|---|---|---|---|---|---|---|

| Kaiser Permanente | 5.0 |  |

HMO, POS, PPO | 23,900+ physicians | Learn More | On Healthcare Marketplace's Website | ||

| Blue Cross Blue Shield |  |

5.0 | |

EPO, HMO, POS, PPO | 1.7 million+ healthcare providers | Learn More | On Healthcare Marketplace's Website | |

| UnitedHealthcare |  |

4.5 |  |

EPO, HMO | 1.5 million+ healthcare providers | Learn More | On UnitedHealthcare's Website |

How Does Small Business Health Insurance Work?

The Affordable Care Act (ACA) defines a small business as a group of no more than 50 full-time employees (FTE), though some states may define it differently.

A small business owner enrolls in a group health insurance plan offered by a private insurance company and then provides their employees the opportunity to enroll in that plan. The employer pays part of their employees’ monthly premiums, while employees typically pay smaller premiums, as well as their deductibles, copays, coinsurance and services not covered by the plan.

Small business owners contract with health insurance companies and decide how many options to provide to employees.

Do Small Businesses Have to Provide Health Insurance?

Small business owners aren’t legally required to provide health insurance to their workers, but there are rules for those who do.

With that said, make sure you understand how your state defines a small business, as it will impact what you are required to provide, should you decide to offer health insurance to your employees.

Small Business Health Insurance Options

Small business owners can buy health insurance for their employees through approved insurance companies with the Small Business Health Options Program (SHOP).

Getting insurance through the SHOP Marketplace allows employers to offer health plans from multiple insurance companies and qualifies them for the Small Business Health Care Tax Credit, which can help with the cost of providing coverage.

Your business must meet these requirements to qualify for the SHOP tax credit:

- Fewer than 25 full-time equivalent (FTE) employees

- Average employee salary is about $56,000 per year or less

- Pay at least 50% of your full-time employees’ premium costs

- Offer SHOP coverage to all full-time employees

Small business owners can also work with a health insurance broker who conducts all plan research and comparisons to find the best plan for your business at no additional charge. Or they can buy directly from a health insurance company.

If you buy coverage through the ACA marketplace, plans are organized by “metal” tiers: bronze, silver, gold and platinum. The tiers differ by premiums and out-of-pocket costs. For instance, bronze and silver plans have low premiums but higher deductibles and coinsurance. Gold and platinum plans have high premiums but lower out-of-pocket costs.

Employers have flexibility in which type of plans they choose to offer their employees.

Small Business Health Insurance Requirements

Small business owners don’t have to provide health insurance benefits to employees. Should they choose to do so, they must meet certain requirements set by the ACA. These requirements can vary by state.

- Inclusivity: Health insurance must be offered to all employees—not just managers or any other subgroup.

- Coverage of essential health benefits: Under the ACA, a health plan offered by a small business owner must include coverage for basics, such as emergency services, pregnancy-related care and services, maternity and newborn care, outpatient care, prescription drugs and more.

- Minimum contribution: The ACA requires small businesses to contribute at least 50% of the monthly premium cost of the plans they offer to qualify for the Small Business Health Care Tax Credit. In addition to these rules, states typically require a minimum percentage of employee participation in health insurance plans offered by small businesses.

How Much Does Health Insurance for Small Business Cost?

The average cost for small business owners is $612 per employee per month and $1,274 for family coverage per month, according to Kaiser Family Foundation’s 2023 Employer Health Benefits Survey.

The exact cost depends on multiple factors, including previous health insurance claims. For instance, a year of high employee healthcare costs could lead to higher health insurance rates set by the insurance company the next year.

How To Get Health Insurance for a Small Business

You have several options when it comes to searching for the right plan options for your small business:

- Do your own footwork: Small business owners can sort through group health insurance options from different insurance companies to compare prices and services and enroll in a plan that meets their needs. Health insurance companies typically offer multiple plans for small businesses. You can see plan choices and costs by plugging a minimal amount of information on the ACA marketplace website.

- Work with an insurance broker: Insurance brokers know the ins and outs of health insurance plans, as well as state and federal requirements. Just be sure you’re working with an independent or agnostic broker who will show you all plans available to you to best meet your needs.

- Explore the SHOP Marketplace: At Healthcare.gov, you’ll find helpful calculation tools and clear choices for high-quality group insurance plans.

How to Compare Small Business Health Insurance Plans

Choosing a small business health insurance plan requires you to act similar to a consumer buying an individual health insurance plan on the Affordable Care Act (ACA) marketplace.

Here’s what to look at when comparing small business health insurance plans.

Benefit design

See what types of health plans a company offers, including:

- Preferred provider organization (PPO)

- Health maintenance organization (HMO)

- Exclusive provider organization (EPO)

- Point of service (POS)

The benefit design dictates whether employees can get out-of-network care and need referrals to see specialists. One employee may like the lower premiums in an HMO and not have a problem staying in-network, while another may prefer the flexibility of a PPO with the understanding that they will pay more in premiums. Providing employees options can help with employee satisfaction.

Premiums

A health insurance premium is what members pay to have coverage. This usually gets deducted from paychecks. Employers pay most of the premiums, so businesses will need to figure out how much coverage will cost them and their employees.

Out-of-pocket costs

Health insurance deductibles, coinsurance and out-of-pocket maximums play vital roles in how much members pay when they need health care services. Choosing a plan with high deductibles may cost businesses and employees for premiums, but it also puts more costs on employees when they need healthcare.

Provider network

Health insurance companies contract with providers and medical facilities like hospitals. These contracts decide how much providers get paid and may set requirements for providers, such as requiring that they meet a minimum quality of care. A small network could result in employees needing to search for a doctor and lead to extra out-of-network costs.

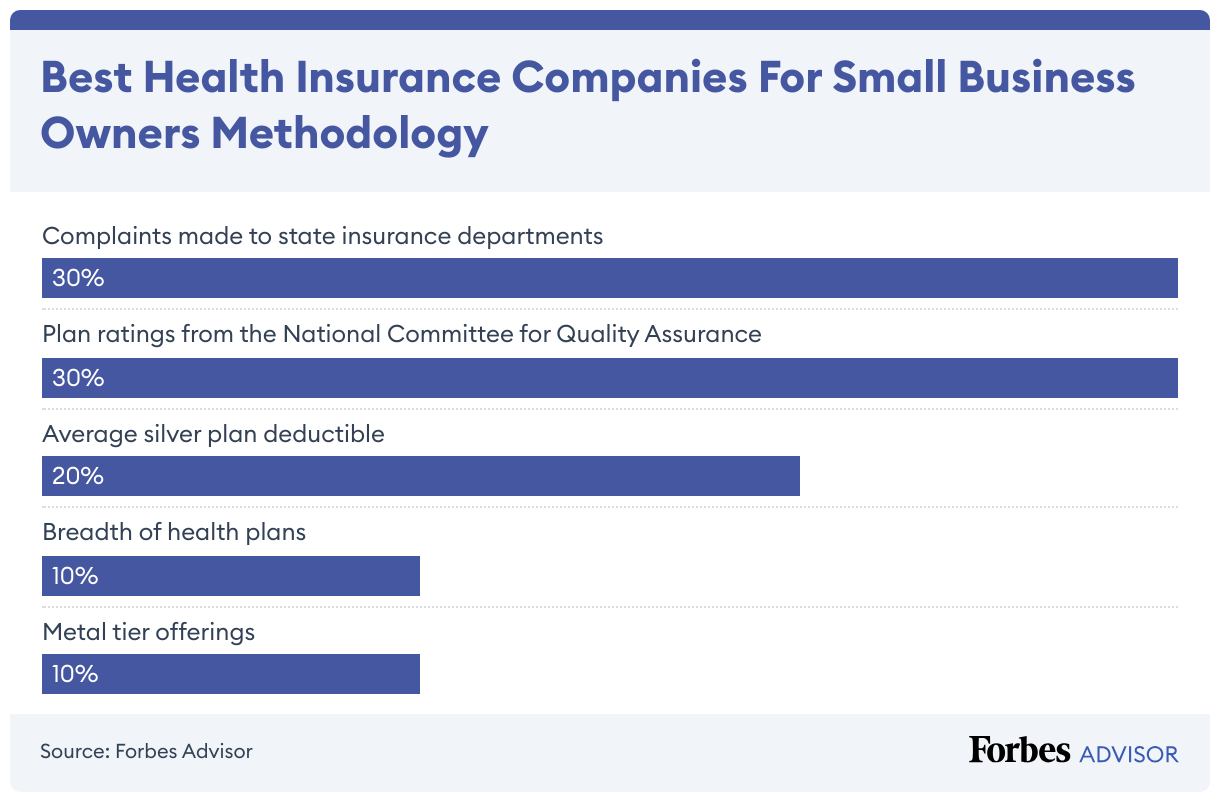

Methodology

We analyzed 84 data points about coverage and quality for seven large health insurance companies to determine the best health insurance providers for small businesses owners. Our ratings are based on:

- Complaints made to state insurance departments (30% of score): We used complaint data from the National Association of Insurance Commissioners.

- Plan ratings from the National Committee for Quality Assurance (30% of score): The National Committee for Quality Assurance (NCQA) is an independent, nonprofit organization that accredits health plans and produces ratings based on specific metrics, including patient experience, prevention, treatment, overall rating of the health plan and rating of care.

- Average silver plan deductible (20% of score): The deductible is how much you have to pay for healthcare in a year before the health plan begins picking up a portion of the costs. Companies with health plans that had low deductibles got more points.

- Breadth of health plans (10% of score): Health insurance companies may offer up to four types of plan benefit designs (PPO, HMO, EPO and POS). Companies that offered more types of plans got more points.

- Metal tier offerings (10% of score): The ACA marketplace has four metal tier levels. We gave points to companies that offered more tier plan options.

Read more: How Forbes Advisor rates health insurance companies

Small Business Health Insurance Frequently Asked Questions

What is a self-insured health plan?

An employer collects health insurance premiums in a self-insured health insurance plan and the business pays the claims rather than a health insurance company. Self-insured plans are more often an option for larger companies.

One potential benefit of self-insured plans is that businesses can save money if they collect more premiums than claims paid out. On the other hand, it could cause a problem if claims exceed premiums.

A self-insured health plan generally still requires that employers contract with a third party to enroll members, process claims and set up provider networks.

How much does group health insurance cost for small businesses?

The average annual cost of health insurance for small businesses is $8,722 annually per employee. Of that amount, employers pick up $7,349 on average and employees pay the rest, according to Kaiser Family Foundation’s 2023 Employer Health Benefits Survey.

Small businesses pay less for health maintenance organization (HMO) plans than other plans. Small companies spend $6,644 annually on average for HMO coverage per employee compared to $6,970 for a point of service (POS) plan and $7,729 for a preferred provider organization (PPO) plan, according to Kaiser Family Foundation.

The Kaiser Family Foundation added that small companies are more likely to pay all employee premiums than larger companies. The report said 30% of covered workers in small firms don’t pay premiums for single coverage for health insurance. That’s compared to just 6% in large companies.

How many employees does a small business have to have to provide health insurance?

Small businesses don’t have to offer health insurance, but employers with more than 50 full-time employees working at least 30 hours per week must offer coverage or face tax penalties.

Small businesses that provide coverage may benefit from tax credits.

Can business owners buy a plan on the marketplace?

Small businesses can buy health coverage for employees on the health insurance marketplace through the Small Health Options Program (SHOP). SHOP lets employers compare plans and the Small Business Health Care Tax Credit can help save money for businesses.