Car insurance is required to drive legally in nearly all states, so it’s helpful to know what you can expect to pay for coverage. Forbes Advisor found the average cost of car insurance is $2,150 for full coverage and $467 for state minimum coverage.

We analyzed rates from the best car insurance companies to find the average cost of auto insurance by:

All of these factors are taken into account by car insurance companies when pricing policies.

Key Takeaways

- The average cost for full coverage car insurance is $2,150 per year. State minimum insurance is 79% cheaper at $467 per year but doesn’t include comprehensive and collision, which pays for damages to your car.

- USAA, Auto-Owners and Geico are the cheapest car insurance companies for full coverage. USAA is only available to drivers with a military affiliation.

- Erie, Mercury and Progressive are the cheapest for state minimum car insurance, according to our analysis of top insurers.

- Idaho, Vermont and Ohio are the cheapest states for full coverage car insurance. The most expensive states are New York, Florida and Louisiana.

How Much Does Car Insurance Cost?

The national average cost for car insurance is $2,150 per year, according to Forbes Advisor’s analysis. This rate is for full coverage car insurance, which includes optional coverage for theft and damage to your own vehicle.

Drivers with the minimum amount of liability car insurance required by their state pay an average of $467 per year, based on our analysis.

Full Coverage vs. Minimum Coverage

Minimum coverage car insurance is a policy that provides the state-mandated amount of liability car insurance you need to drive legally. It’s bare-bones coverage that doesn’t pay for damage to your vehicle, so it’s usually the cheapest type of car insurance.

Depending on what state you live in, a minimum coverage policy may also include uninsured motorists, personal injury protection or medical payments insurance. These are all coverages that, in different ways, pay for medical bills you may incur if injured in an auto accident.

Full coverage car insurance includes liability insurance as well as comprehensive and collision insurance, which help to repair or replace your car. There’s no standard definition of full coverage car insurance, but it generally includes:

- Liability insurance, which pays the cost of others’ injuries and property damage when you cause an accident and for your legal defense, judgments and settlements if you’re sued.

- Collision insurance, which pays for collision damage to your car, regardless of fault.

- Comprehensive insurance, which pays for theft and non-crash damage to your car, such as damage from flooding, fire or striking an animal.

- Uninsured motorist coverage, which pays for you and your passengers’ medical bills if injured in an accident caused by an uninsured driver.

Knowing the difference between full coverage and minimum liability coverage will help you determine which is right for you.

How Much Does Car Insurance Cost In Your State?

Where you live factors into your auto insurance rates. For instance, car insurance companies look at the number of claims in your area and how much they cost, and if your region is prone to severe weather, like flooding and hurricanes, among other things.

Since the likelihood of accidents is typically higher in urban areas where there are more cars on the road, densely populated states generally have higher average car insurance rates than rural states with fewer drivers.Least and Most Expensive States for Full Coverage Car Insurance

Our analysis of average car insurance rates by state finds that Idaho is the cheapest state for full coverage car insurance. The five cheapest states for full coverage auto insurance are:

- Idaho: $1,021 a year

- Vermont: $1,037 a year

- Ohio: $1,112 a year

- Maine: $1,216 a year

- Iowa: $1,238 a year

The most expensive state for full coverage auto insurance is New York. The top five most expensive states for full coverage car insurance are:

- New York: $4,769 a year

- Florida: $4,326 a year

- Louisiana: $3,629 a year

- Pennsylvania: $3,600 a year

- Maryland: $3,349 a year

Least and Most Expensive States for Minimum Liability Car Insurance

Drivers in Wyoming pay the least for minimum liability coverage car insurance compared to the rest of the country. The five cheapest states for state-minimum car insurance coverage are:

- Wyoming: $248 a year

- Vermont: $277 a year

- Iowa: $287 a year

- South Dakota: $288 a year

- Idaho: $368 a year

Michigan drivers pay the most when they buy their state’s minimum liability car insurance. The top five most expensive states for state minimum auto insurance are:

- Michigan: $1,491 a year

- Florida: $1,310 a year

- New Jersey: $1,236 a year

- New York: $1,172 a year

- Delaware: $1,018 a year

Average Car Insurance Rates by State

| State | Average annual full coverage cost | Average annual minimum coverage cost | State minimum liability requirements |

|---|---|---|---|

|

$1,809

|

$497

|

25/50/25

|

|

|

$2,323

|

$381

|

50/100/25

|

|

|

$1,696

|

$604

|

25/50/15

|

|

|

$2,061

|

$511

|

25/50/25

|

|

|

$2,462

|

$758

|

15/30/5

|

|

|

$2,489

|

$483

|

25/50/15

|

|

|

$1,730

|

$805

|

25/50/25

|

|

|

$2,462

|

$1,018

|

25/50/10

|

|

|

$4,326

|

$1,310

|

31/12/1969 | |

|

$2,181

|

$743

|

25/50/25

|

|

|

$1,633

|

$370

|

20/40/10

|

|

|

$1,021

|

$368

|

25/50/15

|

|

|

$2,345

|

$539

|

25/50/20

|

|

|

$1,454

|

$409

|

25/50/25

|

|

|

$1,238

|

$287

|

20/40/15

|

|

|

$1,693

|

$521

|

25/50/25

|

|

|

$1,979

|

$751

|

25/50/25

|

|

|

$3,629

|

$847

|

15/30/25

|

|

|

$1,216

|

$413

|

50/100/25

|

|

|

$3,349

|

$955

|

30/60/15

|

|

|

$2,333

|

$491

|

20/40/5

|

|

|

$2,995

|

$1,491

|

50/100/10

|

|

|

$2,360

|

$610

|

30/60/10

|

|

|

$1,704

|

$487

|

25/50/25

|

|

|

$2,323

|

$618

|

25/50/25

|

|

|

$1,770

|

$391

|

25/50/20

|

|

|

$1,538

|

$415

|

25/50/25

|

|

|

$3,342

|

$858

|

25/50/20

|

|

|

$1,411

|

$402

|

25/50/25

|

|

|

$2,240

|

$1,236

|

25/50/25

|

|

|

$2,104

|

$369

|

25/50/10

|

|

|

$4,769

|

$1,172

|

25/50/10

|

|

|

$1,307

|

$411

|

30/60/25

|

|

|

$1,319

|

$397

|

25/50/25

|

|

|

$1,112

|

$435

|

25/50/25

|

|

|

$2,291

|

$509

|

25/50/25

|

|

|

$1,459

|

$723

|

25/50/20

|

|

|

$3,600

|

$504

|

15/30/5

|

|

|

$2,715

|

$733

|

25/50/25

|

|

|

$2,387

|

$778

|

25/50/25

|

|

|

$1,821

|

$288

|

25/50/25

|

|

|

$1,720

|

$475

|

25/50/25

|

|

|

$2,938

|

$653

|

30/60/25

|

|

|

$1,955

|

$592

|

25/65/15

|

|

|

$1,037

|

$277

|

25/50/10

|

|

|

$1,486

|

$530

|

30/60/20

|

|

|

$1,829

|

$507

|

25/50/10

|

|

|

$1,688

|

$500

|

25/50/25

|

|

|

$1,905

|

$397

|

25/50/10

|

|

|

$1,341

|

$248

|

25/50/20

|

Average Cost of Car Insurance by Age

Car insurance costs start high in your teen years but begin to decrease as you move beyond your teenage years. You’re no longer an inexperienced driver. As long as you keep your driving record clear of accidents or tickets, your rates should get cheaper as you get older, until your late 60s or early 70s when they will start rising.

Average Car Insurance Rates by Age

| Age | Average cost per year |

|---|---|

|

$6,148

|

|

|

$4,500

|

|

| 25 |

$2,461

|

| 30 |

$2,189

|

| 40 |

$2,110

|

| 50 |

$1,971

|

| 60 |

$1,915

|

| 70 |

$2,099

|

| 80 |

$2,574

|

Car insurance rates generally decrease over time from age 18 to 60. For instance, 30-year-old drivers pay 64% less for car insurance than 18-year-old drivers, on average. And at 60, you pay about 13% less for coverage than you do at age 30. But rates start to climb again when you hit your 70s and keep going up as you hit your 80s.

Senior drivers have experience on their side but reaction times may decrease so car insurance companies consider those in their 70s and older to have a higher likelihood of getting into accidents.

Average Cost of Car Insurance for Teens

Teen drivers are inexperienced and get into more accidents than older drivers, which means teen drivers are super expensive to insure. That makes it critical to shop for the best cheap car insurance for teen drivers.

The average car insurance rate for 16-year-old drivers with their own policy is $8,765 a year. Average rates for 17-year-olds clock in at $6,829 a year. That’s about 22% lower than what 16-year-olds pay.

The cheapest way to insure teen drivers is usually by adding them to your policy. Still, it can double the parents’ auto insurance costs. For instance, listing a 16-year-old driver on a parent policy increased the rate by an average of 82%, our analysis found. The annual cost for the parents’ policy jumped from $2,948 to $5,367 a year. That’s a $2,419 increase.

Average Car Insurance Rates for a Parents’ Policy With Teen Added

| Age of teen driver | Parents’ average annual car insurance cost after adding teen driver |

|---|---|

|

$5,367

|

|

|

$5,011

|

|

|

$4,773

|

|

|

$4,443

|

Average Cost of Car Insurance by Company

Each auto insurance company assesses risk differently, which means prices can vary significantly among companies. That’s why comparing auto insurance quotes from multiple companies can help you find the best price for your specific situation.

Average Car Insurance Rates by Company for Full Coverage

The cheapest full coverage car insurance ranges from $1,412 to $3,233 a year, on average, among the companies we analyzed.

USAA, which is one of the best military car insurance companies, is the cheapest but it’s only available if you’re a military member, veteran or military family member. The next cheapest is Auto-Owners ($1,628 a year), followed by Geico ($1,716 a year).

Average Cost of Car Insurance by Company for Full Coverage

| Company | Average annual car insurance cost |

|---|---|

|

$1,412

|

|

|

$1,628

|

|

|

$1,716

|

|

|

$1,759

|

|

|

$1,852

|

|

|

$1,959

|

|

|

$2,041

|

|

|

$2,144

|

|

|

$2,157

|

|

|

$2,176

|

|

|

$2,381

|

|

|

$2,647

|

|

|

$3,000

|

|

|

$3,233

|

*USAA auto insurance is only available to military members, veterans and their families.

A full coverage car insurance policy costs more than a liability-only policy because it provides collision and comprehensive coverage. If your car is leased or financed, your lender will usually require you to carry full coverage auto insurance.

Average Car Insurance Rates by Company for State Minimum Liability Insurance

Average rates for minimum coverage among companies we evaluated start at $241 a year with Erie and Mercury and go up to $892 a year with Safe Auto, a difference of over $651.

Average Cost of Car Insurance by Company for Minimum Coverage

| Company | Average annual car insurance cost for state minimum |

|---|---|

|

$241

|

|

|

$241

|

|

|

$299

|

|

|

$306

|

|

|

USAA*

|

$336

|

|

$374

|

|

|

$412

|

|

|

$430

|

|

|

$487

|

|

|

$511

|

|

|

$576

|

|

|

$589

|

|

|

$846

|

|

|

$892

|

*USAA auto insurance is only available to military members, veterans and their families.

Cheap liability-only car insurance isn’t hard to find, but it doesn’t pay for damage to your own vehicle. If your budget has more room, you can raise your liability limits to decrease the chance of paying a significant amount of money out of pocket if you cause a serious accident. Also consider buying comprehensive and collision insurance if you want to add coverage for damage to your own car.

No matter what type of policy you’re buying, comparison shop for the same coverages and limits to get an accurate picture of which car insurance company is most affordable.

Average Cost of Car Insurance by Driving History

Good drivers pay lower rates than drivers with tickets or accidents on their driving records. Car insurance companies reward those with clean driving records with cheaper rates because good drivers typically file few claims, so are generally cheaper to insure.

Average Car Insurance Rates After a Speeding Ticket

Good drivers (with no tickets or accidents) pay an average of $2,150 annually for full coverage, based on our analysis. But if you get busted for speeding, expect to pay more for car insurance after a speeding ticket—an average annual hike of nearly $500. That brings the average rate after a speeding ticket to $2,633 a year.

Average Car Insurance Rates After a DUI

Car insurance rates after a DUI increase by an average of nearly $1,400 a year—from $2,150 to $3,537 a year, based on our analysis.

Average Car Insurance Rates After an At-Fault Accident

Car insurance rates after an accident increase an average of 40% for drivers who cause property damage. That spikes the average rate by over $850 a year, from $2,150 to $3,005.

Some state laws prohibit one minor accident from triggering a rate hike. For example, in New York, car insurance companies aren’t allowed to raise rates if the total accident damage is less than $2,000 and there are no injuries.

Even when state laws don’t apply, some insurance companies will let a minor accident go without dinging your rates. For instance, in most states Progressive won’t increase rates if your total accident claim is $500 or less.

Many car insurance companies offer an accident forgiveness benefit—as part of being a loyal customer or for a fee—that spares you from a rate increase after your first auto accident. But if you have two accidents, don’t expect a pass on the second one.

Average Cost of Car Insurance Based on Credit

Auto insurance companies say drivers with lower credit are more likely to file claims. That’s why car insurance rates for drivers with poor credit are often very high.

Our analysis found that drivers with poor credit pay about 76% more than drivers with good credit, on average. That’s an average price hike of over $1,600 a year, from $2,150 to $3,779—and that’s for drivers with clean driving records.

Not all states allow your credit to be used in pricing car insurance. Using a credit-based auto insurance score is banned from auto insurance rate calculations in California, Hawaii, Massachusetts and Michigan.

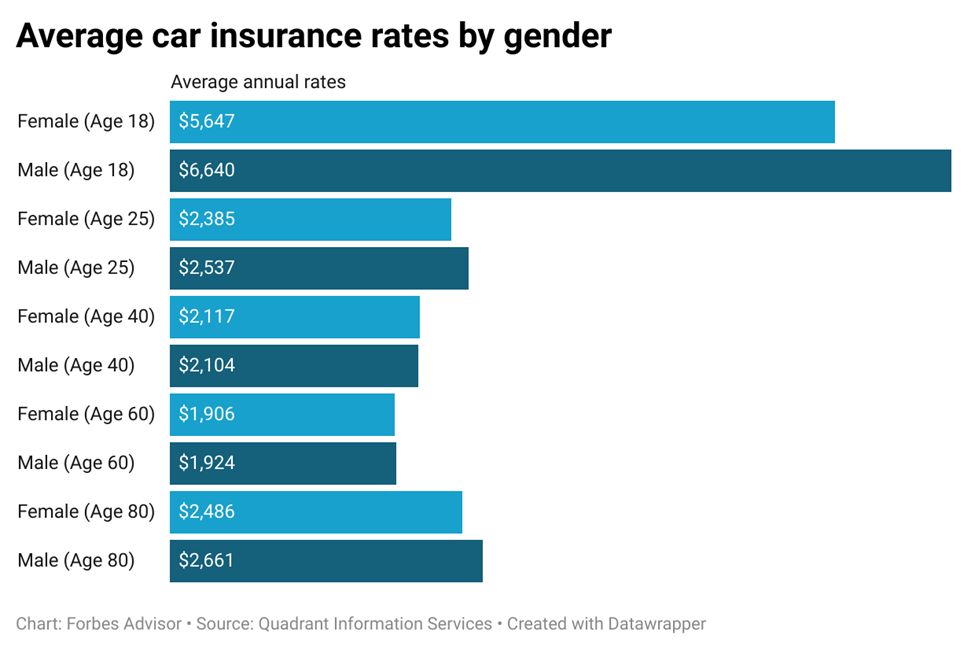

Average Cost of Car Insurance by Gender

Gender can be used as a factor in car insurance rates in all states except California, Hawaii, Massachusetts, Michigan, North Carolina and Pennsylvania.

Car insurance companies find young males more likely to engage in risky driving behavior, so they pay more than females initially. Rates tend to decrease for males after age 25 and become mostly on par with their female counterparts as they get older.

Our analysis of car insurance rates for males and females ages 18 to 80 found that males and females pay about the same amount for car insurance in their middle years. Once males hit their senior years, auto insurance rates start to increase again. The same reasoning from their youth holds true again. Car insurance companies’ actuarial data shows older males exhibit riskier driving patterns than females so they’re charged more for car insurance.

Average Car Insurance Rates by Age and Gender

| Driver's age and gender | Average annual cost | % difference males pay compared to females | $ difference males pay per year compared to females |

|---|---|---|---|

|

Female Age 18

|

$5,657

|

||

|

Male Age 18

|

$6,640

|

17% more

|

$983 more

|

|

Female Age 25

|

$2,385

|

||

|

Male Age 25

|

$2,537

|

6% more

|

$152 more

|

|

Female Age 40

|

$2,117

|

||

|

Male Age 40

|

$2,104

|

‘-0.61% less

|

$13 less

|

|

Female Age 60

|

$1,906

|

||

|

Male Age 60

|

$1,924

|

1% more

|

$18 more

|

|

Female Age 80

|

$2,486

|

||

|

Male Age 80

|

$2,661

|

7% more

|

$175 more

|

Related: How Gender and Age affect Car Insurance Rates

Average Cost of Car Insurance by Car Type

The type of car you drive affects auto insurance rates, particularly collision and comprehensive coverage costs. It’s cheaper to insure vehicles with better safety records and cheaper repair bills and that are less costly to replace if totaled in an accident.

Minivans are the generally cheapest type of vehicle to insure.

Average Car Insurance Rates by Car Type

| Car type | Average annual cost |

|---|---|

|

Minivan

|

$2,041

|

|

Van

|

$2,168

|

|

Trucks

|

$2,234

|

|

Hatchback

|

$2,298

|

|

SUV

|

$2,378

|

|

Sedan

|

$3,184

|

|

Convertible

|

$3,393

|

|

Wagon

|

$3,438

|

|

Coupe

|

$3,894

|

Average Car Insurance Rates by Fuel Type

Hybrid and electric car insurance is more expensive than insurance for gas-powered cars because they can be more expensive to repair. Mechanics may need specialized training and parts can be more costly.

| Car fuel type | Average annual cost |

|---|---|

|

Gas

|

$2,567

|

|

Hybrid

|

$2,802

|

|

Electric

|

$3,547

|

Average Car Insurance Costs for Top-selling Vehicles

The Honda CR-V and Subaru Outback have an average annual rate of $1,723. That’s $1,405 a year cheaper than the insurance cost of the most expensive vehicle on our list.

Tesla Model Y insurance is the most expensive at $3,128 a year, followed by Tesla Model 3 insurance at $3,053 a year. The Tesla Model Y car insurance costs are 82% more than the Honda CR-V or Subaru Outback. The value of the vehicles and repair costs are a couple of reasons the Tesla models are so expensive to insure.

| Rank | Vehicle | Annual average cost |

|---|---|---|

| 1 |

Ford F-150 XL

|

$1,769

|

| 2 |

Chevrolet Silverado 1500 Limited WT

|

$1,812

|

| 3 |

Ram 1500 Classic Express

|

$1,963

|

| 4 |

Toyota RAV4 LE

|

$1,835

|

| 5 |

Tesla Model Y Long Range

|

$3,128

|

| 6 |

Toyota Camry SE

|

$2,095

|

| 7 |

Honda CR-V EX

|

$1,723

|

| 8 |

Chevrolet Equinox LS

|

$1,856

|

| 9 |

Toyota Tacoma SR

|

$1,990

|

| 10 |

GMC Sierra 1500 Pro

|

$1,827

|

| 11 |

Ford Explorer

|

$1,979

|

| 12 |

Tesla Model 3

|

$3,053

|

| 13 |

Jeep Wrangler Sport

|

$1,807

|

| 14 |

Toyota Corolla L

|

$2,099

|

| 15 |

Toyota Highlander LE

|

$1,990

|

| 16 |

Jeep Grand Cherokee Laredo

|

$1,960

|

| 17 |

Hyundai Tucson N Line

|

$1,868

|

| 18 |

Kia Sportage EX

|

$1,831

|

| 19 |

Subaru Outback

|

$1,723

|

| 20 |

Nissan Altima 2.5 SV

|

$2,316

|

Factors That Affect Car Insurance Prices

These main factors that affect car insurance rates are used by most auto insurers, though how each item is weighed varies. That’s one reason auto insurance costs vary among companies and why it’s wise to compare car insurance quotes.

Auto Insurance Coverage and Limit Selections

Optional coverages you include on your policy beyond the state minimum requirements will add to the price you pay, as will higher limits. To keep costs down, make certain the coverages you select match your needs and skip coverages you may not use.

Gender

Males typically see higher costs than females for car insurance when they are young (ages 16 to 25) and older (60 and over) because insurance companies find that they are more likely to be in accidents. But California, Hawaii, Massachusetts, Michigan, North Carolina and Pennsylvania all ban the use of gender as a rating factor.

Vehicle Model

If you drive a car that is expensive to repair, such as a luxury sports car or a new vehicle equipped with high-tech devices, you typically pay more for car insurance than if you drove a car that isn’t costly to fix, all else being equal. Insurers also look at theft rates and claims records for your car model to predict how likely it is that you’ll make a claim. The more risk your car poses, the more you’ll pay for car insurance.

Your Age and Years of Driving Experience

Young drivers under the age of 25 and senior drivers over the age of 65 normally pay more for car insurance. Young drivers pay more due to inexperience and senior drivers because their driving abilities are declining.

Years of driving are considered by insurers because the less experience you have, the more likely you will get into an auto accident. Hawaii doesn’t allow age or driving experience to be used as rating factors.

Your Car Insurance History

Insurance companies see if you’ve had continuous coverage or lapses in coverage. Having continual coverage on your car gets you better prices, while a gap in coverage will cause your rates to rise.

Your Claims History

If you’ve made car insurance claims in the past you generally pay more than drivers who have been free of claims for many years. That’s because car insurance companies categorize drivers with claims as being more costly to insure.

Your Credit Score

Car insurance companies look at your credit-based insurance score and if you have poor credit you’ll see higher rates. Insurers say drivers with poor credit have a higher likelihood of filing claims so adjust rates accordingly. The use of credit in pricing car insurance is controversial because consumer advocates say it’s discriminatory, but only California, Hawaii, Massachusetts and Michigan prohibit this practice.

Your Driving record

A driving record with traffic violations or accidents is a sign to insurers that you’re a risky driver so they will charge you higher rates. A clean driving record will get you better rates and a good driver discount with many auto insurance companies.

Your Location

Your insurance company reviews the frequency and cost of claims in your locale for auto accidents and theft as well as evaluating how susceptible the region is to extreme weather, like flooding, hail storms and hurricanes. You’ll see higher average car insurance costs if your area sees a higher number of claims.

Learn More: Why is my Car Insurance so Expensive?

What Does Car Insurance Cover?

The core types of car insurance help pay for accidents, injuries and non-crash damage to your car.

- Liability insurance: Liability insurance is required in most states and is the base of an auto insurance policy. It pays for property damage and injuries you accidentally cause to others. It also pays for legal fees, judgments, settlements and your defense if you’re sued due to an auto accident.

- Collision insurance: This optional coverage pays to repair or replace your car if you’re in an accident, regardless of fault. Collision car insurance also pays you if you hit an object, such as a pole or a fence.

- Comprehensive insurance: Also optional, comprehensive car insurance covers theft and also pays to repair or replace your vehicle if its damaged by non-crash problems, such as hitting a deer, hail, falling objects, fire, flooding and vandalism.

- Uninsured motorist coverage: Required in some states and optional in others. Uninsured motorist insurance pays you and your passengers’ medical expenses if you’re injured in a car accident caused by a driver without liability car insurance.

- Personal injury protection: Required in some states. Regardless of fault, personal injury protection (PIP) pays your medical bills if you’re injured in an auto accident. PIP also covers your lost wages and replacement services for tasks you can’t perform due to accident injuries, such as child care.

- Medical payments coverage: Medical payments coverage pays for you and your passengers’ medical bills and other types of expenses resulting from an accident, no matter who caused the accident. This coverage is required in some states.

Knowing what car insurance covers is essential to buying a policy that has the best coverage for your particular needs.

Related: Car Insurance Estimator

How to Save Money on Car Insurance Prices

Whether you buy a bare-bones minimum liability car insurance policy or a robust full coverage auto insurance policy, there are ways to find cheap car insurance.

Shop Around with Multiple Companies

The hands-down best way to save money on car insurance is to shop around. Knowing the average cost of car insurance gives you an idea of what you can expect to pay.

But comparison shopping—with at least three auto insurance companies—shows you how much you can save and can identify the companies that offer the best rates.

Ask for Auto Insurance Discounts

Car insurance discounts can be a way to trim your costs. Some price breaks are relatively easy to get—for example, for going paperless. Ask what car insurance discounts you’re eligible for when you want to reduce car insurance costs.

Ask How Much You Can Save by Raising Your Deductible

A deductible is the amount your car insurance company will deduct from an insurance claim check. If you choose a higher deductible, you’ll reduce your car insurance costs because the car insurance company is responsible for paying a little less on claims. Collision and comprehensive coverage each have a deductible.

You can save between 7% to 28% a year on average by increasing your car insurance deductible, according to Forbes Advisor’s analysis of how much you can save by raising deductibles.

Types of Car Insurance Discounts

Discounts help lower the average cost of car insurance. Look for these common discounts and ask your agent if there are any other discounts you’re eligible for to get cheap car insurance.

- Advance shopping discount: Getting quotes before your current policy expires can earn you a discount. It’s best to shop seven to 14 days in advance to receive this savings.

- Defensive driving class. If you’re 55 or older, you may earn a discount for sharpening your skills with an approved driving course. Make sure your insurer approves of a specific course for a discount before taking it.

- Good driver discount: A driving record free of tickets and accidents can qualify you for a good driver discount. Some insurers refer to it as a safe driver discount.

- Membership discount: Ask about a discount based on associations or organizations you’re a member of, such as college alumni associations or a union.

- Multi-policy discount: You can reduce your rates by bundling home and auto policies, meaning you bought them from the same company. Discounts vary between 6% and 23%, according to our research.

- Multi-vehicle discount: Having more than one vehicle on the same car insurance policy gets you a multi-car discount.

- Online quote: Save with some insurers by getting an online quote and then buying a policy.

- Paid in full discount: Pay your car insurance bill upfront instead of paying monthly to save money.

- Paperless discount: Choosing to go paperless with your bills and policy documents may get you a small discount. The discount is usually under 5% but is easy to obtain.

- Vehicle safety features: Some auto insurers give discounts if your car has specific safety equipment, such as airbags, anti-lock brakes or daytime running lights.

If you have a teen or young adult on your policy, ask about:

- Receiving a discount if your child completes an approved driver training program.

- A good student discount if your young driver does well in school (high school or college).

- A reduction in rates for a “student away at school” if your child is off to college at least 100 miles away from home and is without a car.

Related: Best Car Insurance for College Students

Methodology

We used data from Quadrant Information Services, a provider of insurance data and analytics. Unless otherwise noted, average rates are based on a driver with a clean record insuring a Toyota RAV4. Full coverage rates include $100,000 in bodily injury liability coverage per person, $300,000 per accident and $100,000 in property damage liability, uninsured motorist coverage and any other coverage required in the state. The average rates also include collision and comprehensive with a $500 deductible, except where noted. Minimum car insurance rates reflect the minimum amount of auto insurance required in each state.

Best Car Insurance Companies 2024

With so many choices for car insurance companies, it can be hard to know where to start to find the right car insurance. We've evaluated insurers to find the best car insurance companies, so you don't have to.

Average Cost of Car Insurance Frequently Asked Questions (FAQs)

What is the average cost of car insurance?

The average cost of car insurance is $2,150 a year, according to Forbes Advisor’s analysis of full coverage auto insurance policies. The average cost of a basic liability car insurance policy is $467 a year.

Full coverage car insurance includes collision and comprehensive coverage, which pay for damage to your own vehicle due a wide range of problems, from car crashes to floods to fallen tree branches.

What is the average cost of car insurance per month?

The average cost of car insurance is $179 a month for a full coverage policy, according to Forbes Advisor’s analysis. The average cost of state-minimum liability car insurance is $39 a month.

Your own rates will depend on factors such as the vehicle you drive, your driving record and where you live.

How can I get the best car insurance rates?

The easiest way to get the best car insurance rates is to compare car insurance quotes from several insurers. Make sure to compare the same coverage types and limits. Also make sure that the rates you compare include the car insurance discounts you’ll be able to get.