Amy Fontinelle is a freelance writer, researcher and editor who brings a journalistic approach to personal finance content. Since 2004, she has worked with lenders, real estate agents, consultants, financial advisors, family offices, wealth managers, insurance companies, payment companies and leading personal finance websites. Amy also has extensive experience editing academic papers and articles by professional economists, including eight years as the production manager of an economics journal.

Amy Fontinelle

Amy Fontinelle is a freelance writer, researcher and editor who brings a journalistic approach to personal finance content. Since 2004, she has worked with lenders, real estate agents, consultants, financial advisors, family offices, wealth managers, insurance companies, payment companies and leading personal finance websites. Amy also has extensive experience editing academic papers and articles by professional economists, including eight years as the production manager of an economics journal.

Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Reviewed

Chris Jennings

Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

Not all mortgages are created equal. Some mortgage lenders focus on a speedy preapproval process, while others may offer discounts on the interest rate or lower closing costs.

We compared dozens of lenders to come up with this comprehensive list of the best mortgage lenders to make mortgage comparison shopping easier, whether you’re looking to buy a home or are wondering if 2024 will be a good time to refinance an existing mortgage.

Read more

Show Summary

- Best Mortgage Lenders of 2024

- Flagstar Bank: Best Mortgage Lender for Alternative Credit Data Eligibility

- Bank of America: Best Mortgage Lender for Nationwide Availability

- Chase: Best Mortgage Lender for Relationship Discounts

- Guaranteed Rate: Best Mortgage Lender for Fast Closing

- PenFed Credit Union: Best Mortgage Lender for Low Fees

- Rocket Mortgage: Best Mortgage Lender for Flexible Terms

- New American Funding: Best Mortgage Lender for Low Minimum Credit Scores

- PNC Bank: Best Mortgage Lender for Medical Professionals

- Mr. Cooper: Best Mortgage Lender for Interest Rate Discounts

- Truist: Best Mortgage Lender for Applying Online

- Ally Bank: Best Mortgage Lender for Fast Preapproval

- Summary: Best Mortgage Lenders of 2024

- The Complete Guide to Mortgages

- Current Conventional Mortgage Rates

- What Is a Mortgage?

- How Does a Mortgage Work?

- Types of Mortgages

- Credit Score Needed To Get a Mortgage

- Will 2024 Be a Good Time for a Mortgage?

- How To Get a Mortgage & Steps to Take Before Applying

- How To Compare Mortgage Rates

- How To Get Preapproved for a Mortgage

- How To Choose a Mortgage Lender

- Recap: Best Mortgage Companies of March 2024

- Methodology

- Frequently Asked Questions (FAQs)

- Next Up In Mortgages

Best Mortgage Lenders of 2024

- Flagstar Bank: Best Mortgage Lender for Alternative Credit Data Eligibility

- Bank of America: Best Mortgage Lender for Nationwide Availability

- Chase: Best Mortgage Lender for Relationship Discounts

- Guaranteed Rate: Best Mortgage Lender for Fast Closing

- PenFed Credit Union: Best Mortgage Lender for Low Fees

- Rocket Mortgage: Best Mortgage Lender for Flexible Terms

- New American Funding: Best Mortgage Lender for Low Minimum Credit Scores

- PNC Bank: Best Mortgage Lender for Medical Professionals

- Mr. Cooper: Best Mortgage Lender for Interest Rate Discounts

- Truist: Best Mortgage Lender for Applying Online

- Ally: Best Mortgage Lender for Fast Preapproval

Summary: Best Mortgage Lenders of 2024

The Complete Guide to Mortgages

- Current Conventional Mortgage Rates

- What Is a Mortgage?

- How Does a Mortgage Work?

- Types of Mortgages

- Credit Score Needed To Get a Mortgage

- Will 2024 Be a Good Time for a Mortgage?

- How To Get a Mortgage & Steps to Take Before Applying

- How To Compare Mortgage Rates

- How To Get Preapproved for a Mortgage

- How To Choose a Mortgage Lender

- Recap: Best Mortgage Companies of 2024

- Methodology

- Frequently Asked Questions (FAQs)

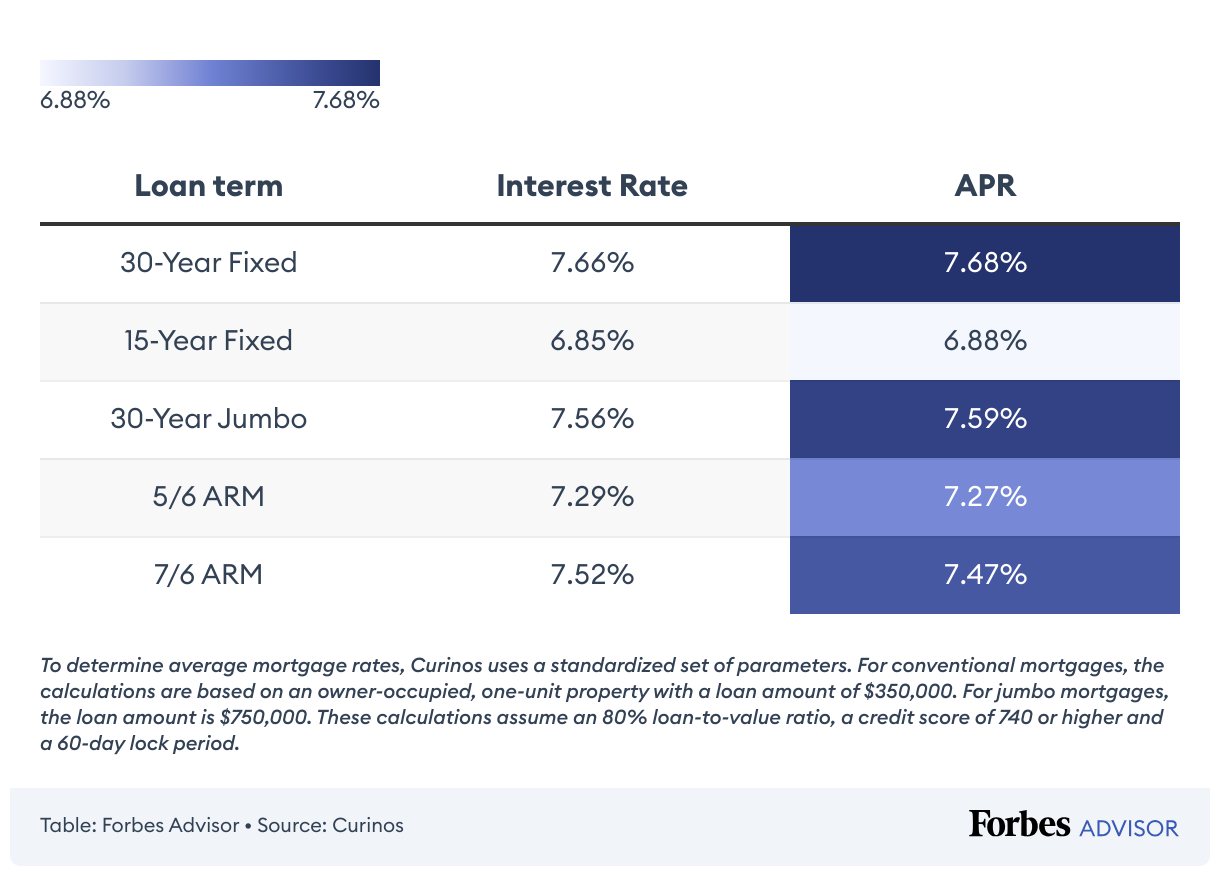

Current Conventional Mortgage Rates

What Is a Mortgage?

A mortgage is a loan secured by property. Most Americans don’t have enough cash to pay for a home, so they take out a mortgage that lasts anywhere from a few years to 30 or more. In exchange, a lender has a lien on the property, meaning that if you fail to make payments, the lender can foreclose and take over the home.

Related: What Is A Mortgage?

How Does a Mortgage Work?

A mortgage works much like any other loan. Your lender gives you money to cover the full cost of purchasing a home, and you pay the money back over a set period of time (usually 15 to 30 years). During this time, you’ll pay back the principal (the original loan amount) plus interest (the fee your lender charges for borrowing).

Mortgages are secured loans, and your home acts as collateral. This means your lender has the right to seize the property—through an act known as foreclosure—if you default on your payments.

Types of Mortgages

There are seven common types of mortgages used to purchase a home: conventional, jumbo, Federal Housing Administration (FHA), Department of Veterans Affairs (VA), United States Department of Agriculture (USDA), 203(k) and non-qualified mortgage (Non-QM).

1. Conventional Mortgage

Conventional mortgages are the most common type of home loan. They aren’t insured by any government agency; instead, they’re funded by traditional banks, mortgage finance companies and credit unions.

Conventional mortgages are often more difficult to qualify for than government home loans, like an FHA loan, but they typically cost less.

2. Jumbo Mortgage

A jumbo mortgage is a loan that exceeds the lending limits set by the Federal Housing Finance Agency (FHFA). They’re used to buy expensive properties and are often reserved for borrowers with strong finances and high credit scores. You’ll typically need to put down a larger down payment with a jumbo loan as well.

The FHFA limit for 2024 is $766,550, meaning you can use a jumbo loan to purchase a home worth more than that in many parts of the country. In high-cost areas, the FHFA limit rises to $1,149,825.

3. FHA Loan

FHA loans are insured by the Federal Housing Administration and issued by approved lenders. They’re intended for homebuyers with low income or those unable to qualify for a conventional loan.

The main benefit of FHA loans is that they have less stringent qualification requirements than conventional loans. Borrowers with a credit score of at least 580 can qualify with a down payment as low as 3.5%. If you have enough to put down at least 10%, you can qualify with a credit score as low as 500. However, depending on how much you put down, you’ll be required to pay mortgage insurance premiums for 11 years or the entire life of the loan.

4. VA Loan

If you’re an active-duty service member or a veteran of the U.S. Armed Forces (or a spouse of one), you might qualify for a mortgage backed by the VA.

As long as you still have full entitlement, you won’t have a VA home loan limit, meaning you won’t have to make a down payment. Those with remaining entitlement must abide by VA home loan limits.

Note that, the VA home loan limit refers to the amount the VA will pay back to the lender if you default on the loan; the VA does not limit how much you can borrow to finance a home.

Like FHA loans, the VA doesn’t issue these loans directly. You’ll need to go through an approved VA loan lender.

Related: What Is a VA Loan?

5. USDA Loan

USDA loans are intended for low- to moderate-income buyers in rural areas designated as eligible by the USDA. There are no down payment or private mortgage insurance (PMI) requirements, but you have to pay a one-time upfront guarantee fee and a recurring annual fee to cover the cost of the loan.

Related: What Is a USDA Loan?

6. 203(k) Loan

A 203(k) loan is insured by the FHA and is intended for those buying a home in need of significant renovations and repairs. A 203(k) loan covers the purchase of the home and the improvements needed. You can’t buy a vacation home or investment property with this type of loan.

7. Non-QM Loan

A non-qualified mortgage, or non-QM loan, is a type of mortgage intended for self-employed buyers or those in unique financial situations. These loans have more flexible credit and income requirements than qualified mortgages.

Credit Score Needed To Get a Mortgage

You’ll typically need a minimum credit score of 620 to qualify for a mortgage. However, government-backed loans like FHA and VA loans tend to have lower minimum credit score requirements than conventional or jumbo loans. Moreover, lenders have the flexibility to establish their own minimum credit score requirements.

Will 2024 Be a Good Time for a Mortgage?

With the economy remaining resilient and inflation stickier than expected, the Federal Reserve has kept its monetary policy on hold. Despite this, the Fed indicated in May that there’s still potential for one to two rate cuts of 25 basis points (0.25%) later in the year.

Although mortgage rates don’t move in lockstep with the Fed’s target interest rate, the Fed’s actions indirectly influence what rates mortgage lenders are willing to offer their customers. Should interest rates fall by about 0.5 percentage points in 2024, per the Fed’s most recent projections, this could lead to big savings on a monthly mortgage payment.

For every $100,000 borrowed, a 0.5 percentage point interest rate decrease would reduce your monthly mortgage payment by $34. On a $350,000 mortgage, for example, your monthly payment will be $119 lower; over the course of a 30-year mortgage, this equates to a savings of nearly $43,000.

Pro Tip

There is no “best time” to purchase a home as real estate fluctuates. However, with mortgage rates elevated, home inventory remaining tight and demand still high, waiting until rates drop to purchase may leave you unable to afford a home. Once rates drop, more people will qualify for home loans, leading to an influx of buyers in the market, potentially opening way to more bidding wars and further driving up the values of homes.

How To Get a Mortgage & Steps to Take Before Applying

Before you even look at applications, you should start the mortgage process by following these steps:

- Check your credit. Make sure there are no errors in your credit report and that everything is up to date. It might be a good idea to spend some time improving your credit.

- Pay down debt. You may also want to take some time to pay down existing debts, since mortgage lenders take into consideration how much debt you already have relative to your income.

- Prepare the paperwork. To apply, you’ll likely need your W-2s, tax returns, recent pay stubs and statements from accounts showing your assets and liabilities. Most lenders will ask for additional information, as well.

- Find a lender. When you’re ready, shop around for the best mortgage lender. You can start with lists like the one above. Consider getting one or more mortgage preapprovals to help make you a stronger buyer when you’re ready to start house-hunting. In addition, ask for a Loan Estimate so that you can compare lenders and their total costs.

Related: How To Get A Mortgage

How To Compare Mortgage Rates

When you apply for a mortgage with multiple lenders, you’ll be able to compare rates and fees, which could save you thousands of dollars. Use these tips to make accurate comparisons:

- Apply on a single day. Since mortgage rates change daily, you won’t be able to tell which lender offers the best rate for your circumstances unless you submit all your applications to different lenders on the same day.

- Apply for the same type of loan. Interest rates can vary by loan type, so you’ll get the best information by applying for the same loan type and term with each lender. In other words, don’t apply for a 15-year FHA loan with one lender and a 30-year conventional loan with another.

- Compare points. One lender might charge you mortgage points for the same interest rate that another lender will give you without points. Check the first section of your loan estimate for this cost. Lenders are often willing to adjust the points and interest rate in your loan estimate within a range that still allows you to qualify.

- Consider the big picture. Loan fees can vary by hundreds or thousands of dollars among lenders. The longer you plan to keep your mortgage, the less important the fees are and the more important the interest rate is. If you expect to move or refinance in a few years, consider keeping your fees as low as possible even if it means a slightly higher interest rate.

How To Get Preapproved for a Mortgage

Applying for a mortgage preapproval isn’t hard. You can do it online, by phone or in person, depending on the lender. Follow these general steps:

- Provide personal information. Lenders need your name, address, phone number and Social Security number or individual taxpayer identification number (ITIN). Be prepared to show your driver’s license or other state-issued ID as well.

- Authorize the lender to pull your credit report. Lenders need your permission to do a hard credit check because it can have a small impact on your credit score.

- Provide proof of income and assets. Copies of documents such as recent paystubs, W-2s, tax returns and bank statements help demonstrate your financial stability and ability to repay the loan.

Once the lender has reviewed your information, they’ll decide whether to offer you a loan and how much you can borrow. The more information they look at up front, the more confidence you can have that there won’t be any unpleasant surprises later. With a mortgage preapproval letter, home sellers will know you’re a serious buyer.

How To Choose a Mortgage Lender

You can choose a mortgage from all kinds of financial institutions, including banks, credit unions and online mortgage lenders like Rocket Mortgage and loanDepot. But you can also work with a mortgage broker, who will do the work of shopping around for the best rate and terms for you.

It’s probably a good idea to look for a lender just before you start house-hunting, so you have a better sense of how much you can afford and whether you’ll be preapproved. Compare multiple lenders rather than going with the first one you find.

What should borrowers consider when choosing a mortgage lender?

Fred Chilton

Advisory Board Member

Scott Bridges

Advisory Board Member

Chris Jennings

Mortgages & Loans Editor

Selecting the right mortgage lender is crucial to securing favorable terms that align with your financial needs. Here are some key things to consider:

- Customer service and reputation. While rates and fees are important, the quality of service is paramount. Consider how responsive and knowledgeable the loan officer is. Are they readily available to address your questions, or do responses lag? Effective communication and expert guidance are essential for a smooth transaction.

- Closing time. Efficiency in closing your loan can be a game-changer. Some lenders may require over 45 days to close, even in less busy periods. Aim for lenders who can complete the process within 21 to 30 days. This swiftness avoids potential hiccups and strengthens your position as a buyer when making an offer on a property.

- Rates and fees. While rates generally are competitive across lenders, the fees or “points” associated with these rates can vary significantly. It’s important to scrutinize these fees as they reflect the lender’s built-in margin and can impact the overall cost of your mortgage.

Fred Chilton

Advisory Board Member

Choosing a mortgage lender is a crucial decision when financing a new home or refinancing an existing loan. While finding the lowest interest rate is important, it’s not the only factor to consider. Here are some other essential elements to keep in mind:

- Exceptional customer service. Look for a lender with a reputation for responsiveness, clear communication and overall positive customer experiences. A dedicated loan officer who promptly answers your questions can make the home financing process much less stressful.

- Technology. Having strong technology that allows you to apply online, upload documents via a secure portal and check the status of your loan is a big plus.

- Breadth of products and guideline expertise. Mortgage guidelines can be complex, so choose a lender with deep knowledge of various loan programs and a full product menu (i.e. conventional, FHA, VA, USDA and home equity loans). They’ll help you find the perfect combination of program type, term length, down payment and interest rate to suit your unique needs.

- Reliable servicer. Mortgage loans often change hands between servicers after closing. Some lenders retain servicing rights, providing a seamless experience with a consistent point of contact. This familiarity can significantly reduce stress and ensure your escrow account and payments are handled responsibly.

Scott Bridges

Advisory Board Member

Don’t settle for one lender. There are a lot of different mortgage lenders out there, and many offer different products and services that might fit your needs better. Try to get at least three preapprovals from different lenders. This will give you an idea of the loan amounts and interest rates you qualify for, and it can potentially save you thousands of dollars. Wait until you’ve made an offer on a home and compared the Loan Estimates from each of your potential lenders before deciding on which one to work with.

Chris Jennings

Mortgages & Loans Editor

Recap: Best Mortgage Companies of March 2024

- Best Mortgage Lender for Alternative Credit Data Eligibility: Flagstar Bank

- Best Mortgage Lender for Nationwide Availability: Bank of America

- Best Mortgage Lender for Relationship Discounts: Chase

- Best Mortgage Lender for Fast Closing: Guaranteed Rate

- Best Mortgage Lender for Low Fees: PenFed Credit Union

- Best Mortgage Lender for Flexible Terms: Rocket Mortgage

- Best Mortgage Lender for Low Minimum Credit Scores: New American Funding

- Best Mortgage Lender for Medical Professionals: PNC Bank

- Best Mortgage Lender for Interest Rate Discounts: Mr. Cooper

- Best Mortgage Lender for Applying Online: Truist

- Best Mortgage Lender for Fast Preapproval: Ally

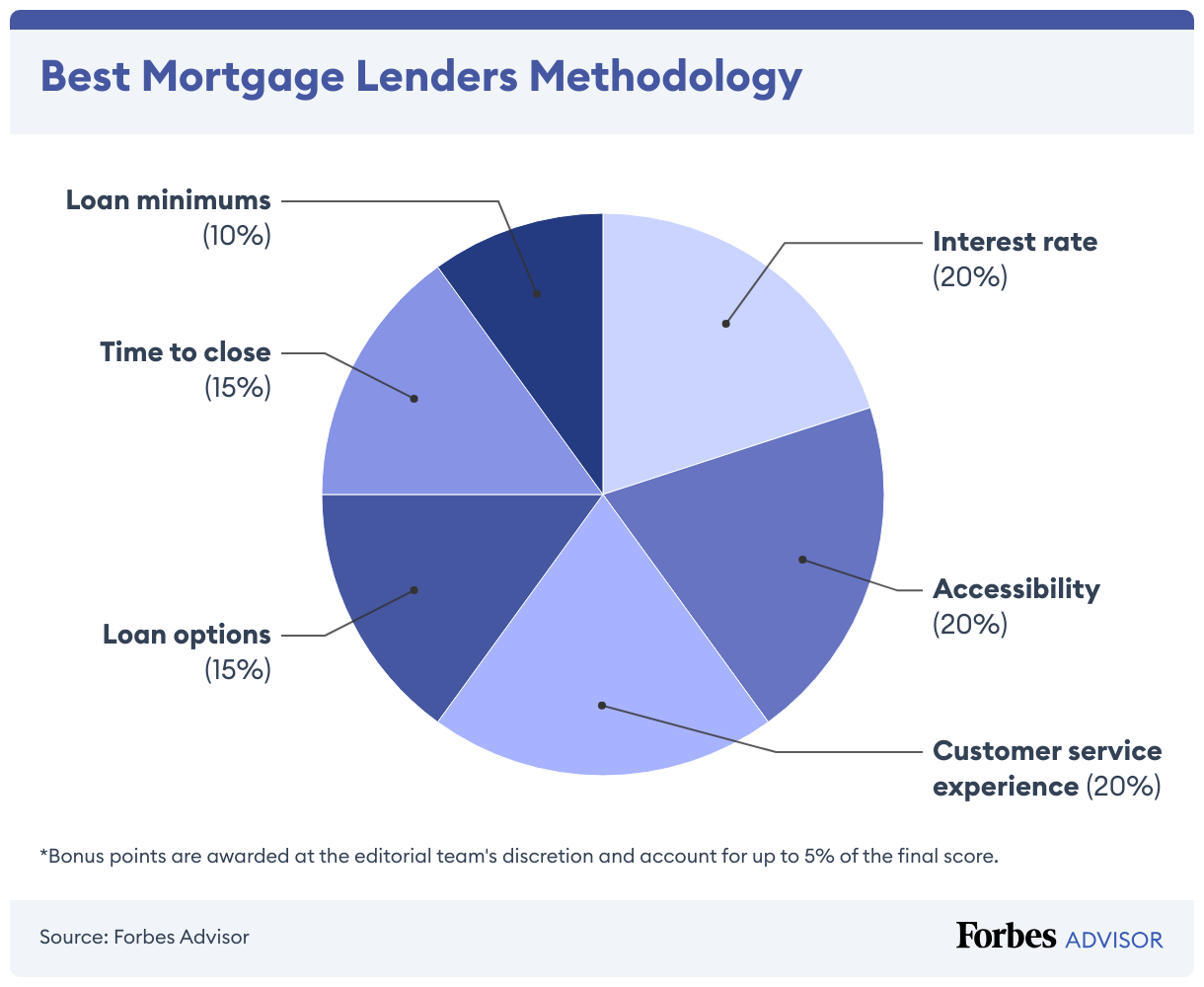

Methodology

Forbes Advisor graded the best mortgage lenders based on features that have a meaningful impact on the cost of a mortgage and a borrower’s experience, including interest rates, loan options, accessibility, closing time and customer service.

We award bonus points if a lender offers a specialty mortgage product, rate discount or considers alternative credit data when determining loan eligibility.

Our scoring method is broken down as follows:

- Interest rate. 20%

- Accessibility. 20%

- Customer service experience. 20%

- Loan options. 15%

- Time to close. 15%

- Loan minimums. 10%

- Bonus points. Up to 5% of the total score

We chose to focus on these core elements to bring forward lenders that offer the most competitive rates while also providing a satisfactory customer experience accessible to borrowers of all financial backgrounds. We believe this scoring system best reflects consumers’ top priorities when comparison shopping for mortgage lenders.

To learn more about our rating and review methodology and editorial process, check out our guide on How Forbes Advisor Reviews Mortgage Lenders.

Frequently Asked Questions (FAQs)

How much house can I afford?

The first step to finding out how much house you can afford is determining your budget. Consider how much you earn each month and how much you spend (on debt, savings, retirement, college funds, etc.).

Most experts recommend spending no more than 30% of your gross monthly income on your mortgage. That should also include taxes, insurance, and applicable HOA fees. The Forbes Advisor affordability calculator will help you take the guesswork out of how much you should spend on a house.

What is private mortgage insurance (PMI)?

Private mortgage insurance, also known as PMI, protects the lender in the event that you default on your mortgage. Typically, if you make a down payment of less than 20% of your home’s purchase price, you will be required to pay PMI. How much you’ll pay for this insurance will vary depending on factors that include the size of your down payment and your credit score.

Mortgage rates vs. APR: What’s the difference?

Mortgage interest rates are what it costs to service your loan. Interest is usually expressed annually for mortgages. The current 30-year, fixed-rate mortgage has an average interest rate of 6% or more.

In contrast, the annual percentage rate, or APR, includes not just the interest rate, but also other finance costs, including fees. This offers a more complete view of the total cost of your loan.

What are the steps to getting preapproved for a mortgage?

Mortgage preapproval represents a lender’s offer to loan the buyer money based on certain financial circumstances and specific terms.

To start the process, begin by gathering documents your lender needs, including a copy of your Social Security card, recent W-2 forms, pay stubs, bank statements and tax returns. The mortgage lender you choose will then guide you through the entire preapproval process, as it can vary depending on the company you plan to borrow from.

Where is the best place to get a mortgage?

There are many options when it comes to finding the right mortgage—from banks and credit unions to online mortgage lenders. Generally, the best place to get a mortgage is from a lender with a mortgage rate and terms that are right for you. In addition to interest rates, make sure to compare fees, credit requirements and available repayment terms.

How do I get the best mortgage rate?

Getting the best mortgage rate always starts with getting your credit as strong as it can be. Start by checking your credit score and addressing any problems. Then work on making yourself look more attractive to mortgage lenders by paying off excessive debt, making sure you make all payments on time and so on.

You should also work on saving for a down payment—the more you save, the less you have to borrow. And avoid making any big life changes like switching jobs or taking on additional credit before your home purchase is complete.

Lastly, you’ll want to start watching mortgage rates on a regular basis and shopping around for lenders.

Related: How to Get the Best Mortgage Rate