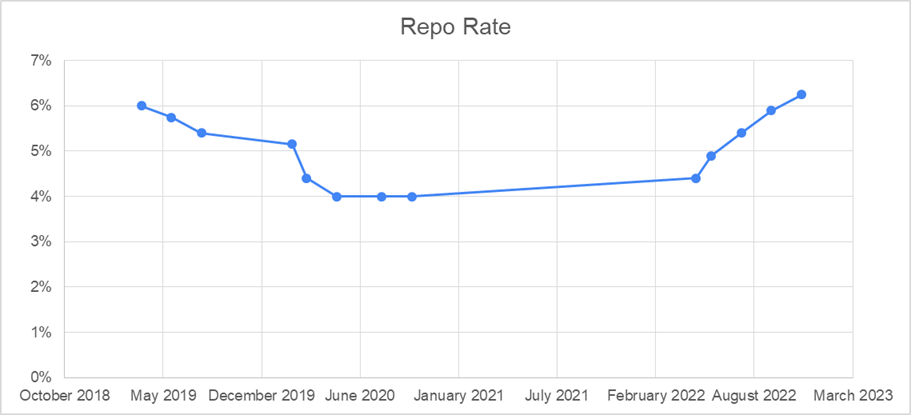

After the latest hike by the Reserve Bank of India, the repo rate currently stands at 6.25%, the exact level as it was in February 2019. From May 2020 to May 2022, the repo rate remained unchanged at 4%. The recent upward movement commenced from May 2022 onwards i.e. when the apex bank decided to control the prevailing inflationary trends in the economy.

Most of us are likely to have unanswered questions around the significance and gyrations of the repo rate. Here’s a primer on what repo rate is and how it works.

What is Repo Rate

Every country’s economy is driven by “policy rates”. In simple words, policy rates are the monetary tools of the central bank that are utilized to control the money supply, to maintain appropriate day to day liquidity in the system, and thereby determine operating bank rates.

Key policy rates and reserve ratios:

● Repo rate, or repositioning rate

● Reverse repo rate

● Cash reserve ratio (CRR)

● Statutory lending ratio (SLR)

1. Repo rate

Repo rate is the interest rate at which the RBI lends to banks in the country. The repo rate increases are intended to make credit costlier; banks generally pass on the increased costs to customers and loans become costlier. Expensive credit dampens consumer demand, resulting in a corresponding drop in demand for goods and services.

Contrarily, reduced repo rates are designed to enhance the availability of funds for banks, thus reducing the overall cost of credit and boosting consumer demand. Consequently, the repo rate is one of the monetary tools to either control inflation or stimulate demand.

In October 2019, the RBI mandated banks link their lending rates to external benchmarks. A majority of banks selected repo rate as their external benchmark. Repo rate, therefore, influences rates of interest on all loans such as personal loans, car loans, housing loans, working capital, among others. There is also the inevitable follow-on impact on rates of fixed deposits and saving accounts.

Repo Rate: April 2019 – December 2022

When the coronavirus pandemic struck, the RBI decided to repeatedly slash repo rates till they bottomed at 4% in May 2020 in an effort to stimulate demand and maintain sufficient liquidity; the same repo rate remained unchanged for two years. The reduction in repo rate did substantially boost liquidity. Whether rock-bottom repo rates translated into enhanced demand stimulus, remains debatable.

The recent hikes have restored the repo rate to pre-Covid levels. Essentially, the RBI is now tightening the money supply to control inflation. Will this be enough? Monetary policy does have limits to its effectiveness.

2. Reverse repo rate

It is the rate of interest at which banks place their money with the RBI. All banks are mandated to maintain statutory reserves with the RBI as per the stipulated cash reserve ratio and the statutory liquidity ratio (SLR).

Banks frequently generate surplus cash, which can also be deposited (at varying tenors) with the RBI. The reverse repo rate is, therefore, interest earned by banks from funds placed with the RBI.

3. CRR

CRR, also called the cash reserve ratio, is the share of a bank’s total deposit that is mandated to be maintained with the RBI (interest-free) as a reserve in the form of liquid cash. The primary purpose of the CRR is to encourage prudence and conservatism in banking operations and to also control the liquidity in the system as a whole.

CRR can be leveraged to control inflation or to act as a demand stimulant. Currently, the CRR is set at 4.5%.

4. Statutory Liquidity Ratio

Every bank must have a specified portion of their net demand and time liabilities (NDTL) in the form of cash, gold, or other liquid assets by the day’s end. A time liability has to be repaid to the customer after a specific time period (fixed deposits) and a demand liability (saving and current accounts) is to be immediately paid as per customer instructions.

It is mandated that commercial banks have to maintain this reserve requirement in the form of liquid cash, gold reserves, government bonds and other RBI approved securities.

The ratio of the above reserve requirement to the demand and time liabilities is called the statutory liquidity ratio (SLR). Currently, the SLR is at 18%; the Reserve Bank of India has the authority to increase this ratio as much as 40%.

Akin to the CRR, the SLR tool mitigates imprudent functioning and ensures that the bank maintains a minimum level of liquidity against their operational liabilities. Both of these tools are frequently employed to either curb inflation or to energize growth.

Currently with the CRR at 4.5% and SLR at 18%, for every deposit of INR 100, the bank can utilize only INR 77.50 for commercial purposes.

How Repo Rate Impacts a Consumer

Changes in macroeconomic policy influences all lives, albeit in varying degrees. The repo rate movements will touch fixed deposit holders as much as the borrowing segment.

In a rising repo rate regime, as banks increase their lending rates, the individual consumer will be faced with tough decision making in the form of higher (unaffordable) equated monthly installments (EMIs), which can dissuade home buyers, leading to unsold housing inventories.

Example: Effect of repo rate increases on an EMI of a INR 50 lakh home loan of a 20-year tenure

The dilemma that a borrower will now face is whether to go with a vastly increased loan tenure, or shoulder a much larger EMI burden.

Below are two scenarios which illustrate the severe dilemma for a Home Loan amount of ₹50 Lakhs.

Scenario One: Tenure is constant and the EMI is increased

Assumptions – At 6.6% vs. 8.65% for a 20-year tenure

The EMI increment of INR 6,293 to the base EMI means you will now have to payout an extra INR 15 lakh during the 20-year tenure of the home loan.

Scenario Two: EMI is kept constant and tenure is increased

Maintaining an unchanged EMI and instead increasing the loan tenure would be very expensive and also completely untenable in most cases as much as 360 months is the maximum tenure offered by lending institutions.

The recent hikes in the repo rate is an indicator of the upward trend, which could possibly continue. As a result, you can expect an enhanced rate of interest on loans and increased EMIs in upcoming months. Accordingly, it is advisable for borrowers to partly repay the loan and/ or increase their EMIs to lower the interest burden. In such a scenario, limiting discretionary spending and avoiding availing unnecessary credit proves to be fruitful.

Global Economy Influence on Repo Rate

Over many decades, the RBI has proactively leveraged policy rates to either control inflation or to fuel growth. However, the RBI has to sometimes set rates in a reactive manner to maintain its tandem with global policy rates. The below graph emphasizes four distinct events.

History of repo rates in India

- In 1991, high inflation plus the economic reforms necessitated a market oriented monetary policy, leading to an immediate increase in repo rates.

- From 2001 to 2004, repo rates were gradually reduced as a follow-up to the dot-com bubble burst.

- Reacting to the global financial crisis of 2008, repo rates were reduced by 1.25%.

- Pandemic-induced economic disruption required immediate demand stimulus. Repo rates were maintained at record lows of 4% for over two years.

- In recent months, rampant inflation is sought to be controlled through a steadily rising repo rate regime.

Like India has repo rates, other countries like the United States and United Kingdom have their own designated policy rates. In a globalized economic order, interconnected financial markets veritably ensure that most countries’ monetary policies mirror each others’. It is inconceivable (though not impossible) to envisage a situation where policy rates in India would move in the opposite direction to those in the U.S. or the UK.

During the pandemic, every country slashed their benchmark rates swiftly and substantially, thereby making money cheaper in their respective economies. Similarly, global central banks together initiated the process of controlling inflation by increasing rates from the middle of 2022; it is a continuing dynamic. The closely coordinated trends in policy rates of three major economies as under:

Bottom Line

Monetary policy rates are an effective tool to realize a nation’s macroeconomic objectives in balancing growth and inflation. Rates can be rationalized quickly, but the results thereof are evidenced over a period of time. Monetary policy is only one of the several tools that are available to decision makers, and as such effectiveness of monetary policy is best enhanced when all other connected measures (example: fiscal policy) are implemented in conjunction.