If you’re planning to purchase a second home or refinance an existing one, current second home mortgage rates can significantly impact your finances. These rates are typically higher than primary residences due to the additional risk posed by second home ownership.

What Are Second Home Mortgage Rates?

Second home mortgage rates are interest rates for financing a second home—a property other than your primary residence. These rates can be fixed—a stable interest rate for the life of the loan—or adjustable—a rate subject to change based on market conditions.

When shopping for a second home, keep an eye on available mortgage rates, as they will significantly impact the overall cost of your investment. By securing a lower interest rate, you can save thousands of dollars over the life of the loan and make your second home more affordable in the long run.

Current Second Home Mortgage Rates

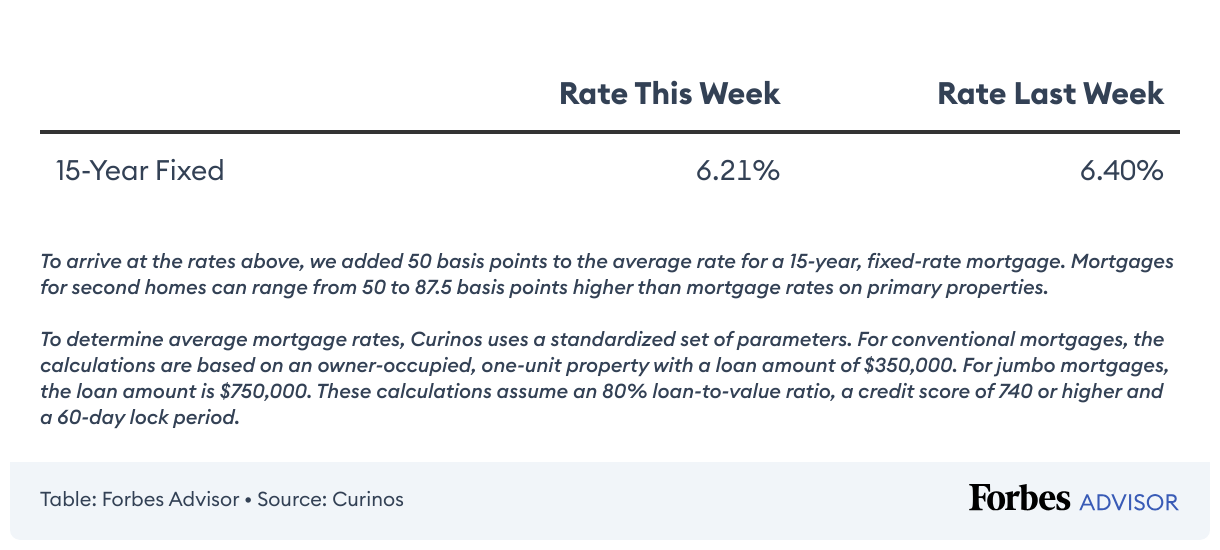

Current 15-Year Second Home Mortgage Rates

Current 30-Year Second Home Mortgage Rates

How To Get a Mortgage for a Second Home

Every financial institution has its own process for applying for a second home mortgage. However, there are a few general steps to follow:

- Calculate affordability. Before buying a second home, determine your budget and factor in potential maintenance costs, insurance and other expenses.

- Get preapproved for a mortgage. Obtaining preapproval will suggest the amount you qualify for. Not only is this important when shopping around for a second home loan, but a preapproval letter can also help you get a house under contract.

- Find the best rate. Shop around to find the lowest interest rates available from reputable lenders. Then, compare the closing costs of each loan option before making your final decision.

- Make an offer. Once you identify a property that fits your budget, make an offer and begin securing financing for your second home.

- Apply for the mortgage. Submit all requested documents for income verification, credit score review, taxes and other pertinent information needed by lenders during this stage of the approval process.

- Close on your loan. After approval, sign all necessary documents to finalize the mortgage and take ownership of your new home.

How To Qualify for a Mortgage on a Second Home

Each lender has unique criteria when approving a loan, so it’s always best to contact a qualified mortgage professional for more information. However, there are several factors that the best mortgage lenders consider when evaluating mortgage applications, including:

- Credit score. You should have a minimum credit score of at least 640 to qualify for a mortgage on a second home. This requirement varies by lender and loan type, but the most competitive interest rates and loan terms are typically reserved for the most creditworthy borrowers.

- Income verification. Lenders require proof of income through pay stubs, W-2 forms and tax returns to verify your ability to cover additional costs associated with owning two properties.

- Employment history. Mortgage providers may also verify that your employment history is sufficient and stable enough to support your debt obligations. A lender may also consider whether you have other steady income sources available.

- Down payment. Most lenders typically require larger down payments for a second home purchase. You should expect to make a down payment of between 10% and 20% of the home’s purchase price.

- Debt-to-income (DTI) ratio. Your DTI ratio is used by lenders to measure how much debt you have relative to your gross monthly income. Lenders typically look for a DTI below 43% for loan approval.

- Reserves. Lenders may require enough cash in reserve to cover at least six months of second home mortgage payments should an emergency arise.

Pros and Cons of a Second Home Mortgage

Second home mortgages can be beneficial if you want to invest in a vacation home or short-term rental. However, it’s important to fully understand this type of financing before choosing a lender—or committing to a loan. These are the main advantages and disadvantages of getting a second home mortgage.

Pros

- Build equity in a second property. A second home mortgage makes it easier to purchase a second property and can help you build equity over time.

- Tax deductions. The interest paid on mortgage payments for your second home may be tax deductible in some cases, which could significantly reduce your total costs.

- A new revenue stream. If you choose to rent out the property, you can create additional income streams to offset the cost of mortgage payments.

Cons

- Higher interest rates. Mortgage rates for second homes are generally higher than those for primary residences.

- Higher down payment requirements. Lenders typically require a higher down payment for second home mortgages than for primary residences.

- Higher taxes and insurance. Beyond typical home expenses, you’ll need to factor in taxes, insurance, maintenance fees and other expenses for your second property.

Faster, easier mortgage lending

Check your rates today with Better Mortgage.

Should You Get a Second Home Mortgage?

A second home mortgage can be a great way to acquire a property for vacation or rental purposes. However, it’s essential to consider a few factors before committing to a second mortgage. First, assess your financial situation to determine the affordability of additional monthly payments. You should also consider associated costs, such as insurance, property taxes and maintenance.

Second, consider the current housing market and the potential for property resale value. Last, reflect on whether you intend to use the property yourself or as an investment. By evaluating these aspects and seeking professional advice, you’ll be more equipped to make an informed decision and determine whether a second home mortgage is the right choice.