Penny Gusner is a senior insurance writer and analyst at Forbes Advisor. For more than 20 years, she has been helping consumers learn how insurance laws, data, trends, and coverages affect them. Penny enjoys translating the complexities of insurance into easy-to-understand advice and tips to help consumers make the best choices for their needs. Her work has been featured in numerous major media outlets, including The Washington Post and Kiplinger’s.

Penny Gusner

Penny Gusner is a senior insurance writer and analyst at Forbes Advisor. For more than 20 years, she has been helping consumers learn how insurance laws, data, trends, and coverages affect them. Penny enjoys translating the complexities of insurance into easy-to-understand advice and tips to help consumers make the best choices for their needs. Her work has been featured in numerous major media outlets, including The Washington Post and Kiplinger’s.

Ashlee is an insurance editor, journalist and business professional with an MBA and more than 17 years of hands-on experience in both business and personal finance. She is passionate about empowering others to protect life's most important assets. When Ashlee isn't spreading insurance knowledge or solving television murder mysteries, she enjoys spending time with her family (including the furry and feathery ones) on their farm in Kentucky.

Fact Checked

Ashlee Valentine

Ashlee is an insurance editor, journalist and business professional with an MBA and more than 17 years of hands-on experience in both business and personal finance. She is passionate about empowering others to protect life's most important assets. When Ashlee isn't spreading insurance knowledge or solving television murder mysteries, she enjoys spending time with her family (including the furry and feathery ones) on their farm in Kentucky.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

In most states, drivers with poor credit will suffer with high car insurance rates. Auto insurance companies correlate lower credit with a higher chance that you’ll make an insurance claim. In anticipation of these claims, they generally charge much higher rates to poor credit drivers.

That doesn’t mean you can’t still look for the best insurance for your situation. We evaluated cost, coverage and complaints to find the best car insurance for drivers with bad credit.

Read more

Show Summary

- Compare Car Insurance Companies

- Best Car Insurance For Drivers With Bad Credit Of 2024

- Summary: Car Insurance for Drivers With Bad Credit

- Cheapest Car Insurance Rates With Bad Credit

- Cheapest Car Insurance Rates for Drivers With Poor Credit in Your State

- Why Do Insurance Companies Look at Your Credit Score?

- How Credit Score Affects Car Insurance Rates

- What Is No Credit Check Insurance?

- How to Save on Car Insurance if You Have Bad Credit

- Methodology

- Car Insurance for Drivers With Bad Credit FAQ

- Next up In Car Insurance

Compare Car Insurance Companies

Best Car Insurance For Drivers With Bad Credit Of 2024

- Nationwide – Good for Usage-based or Mileage-based Insurance

- USAA – Best for Military Members & Veterans

- American Family – Best for Low Level of Complaints

- Geico – Best Car Insurance Rates for Drivers with Poor Credit

- Westfield – Best Family Discounts

- Travelers – Best Price for Gap Insurance

Summary: Car Insurance for Drivers With Bad Credit

| Company | Forbes Advisor Rating | Average annual cost for drivers with bad credit | Level of complaints | LEARN MORE | ||||

|---|---|---|---|---|---|---|---|---|

| Nationwide |  |

5.0 |  |

$2,771 | Very low | Get Quotes | Compare rates via EverQuote’s website | |

| USAA |  |

5.0 |  |

$2,594 | Average | Get Quotes | Compare rates via EverQuote’s website | |

| American Family |  |

4.5 |  |

$3,360 | Very low | Get Quotes | Compare rates via EverQuote’s website | |

| Geico |  |

4.5 | |

$2,426 | Average | Get Quotes | Compare rates via EverQuote’s website | |

| Westfield |  |

4.5 | |

$2,964 | Very low | Get Quotes | Compare rates via EverQuote’s website | |

| Travelers |  |

4.0 |  |

$3,381 | Very low | Get Quotes | Compare rates via EverQuote’s website | |

| Allstate |  |

2.5 |  |

$4,028 | Low | Get Quotes | Compare rates via EverQuote’s website | |

| Farmers |  |

2.5 | |

$3,921 | Low | Get Quotes | Compare rates via EverQuote’s website | |

| Auto-Owners |  |

2.0 |  |

$4,217 | Low | Get Quotes | Compare rates via EverQuote’s website | |

| Progressive | 2.0 | |

$4,215 | Low | Get Quotes | Compare rates via EverQuote’s website |

Cheapest Car Insurance Rates With Bad Credit

Our analysis revealed that Geico has the cheapest average car insurance rates for drivers with bad credit. But because the cheapest company for you can vary by many factors, it’s smart to get car insurance quotes from at least a few companies.

Cheapest Car Insurance Rates for Drivers With Poor Credit in Your State

Our analysis shows that Idaho has the lowest average rates for drivers with poor credit. New York has the highest rates for drivers with poor credit. But as you’ll see below, you can find insurers that offer prices well below your state’s average. That’s why it’s so important for drivers with poor credit to shop around for car insurance.

The use of credit as a pricing factor is prohibited in California, Hawaii, Massachusetts and Michigan.

Why Do Insurance Companies Look at Your Credit Score?

Car insurance companies often rely on what’s known as a “credit-based insurance score” when setting your car insurance rates. Credit-based insurance scores put different weights on different factors compared to a typical credit score, such as a FICO score.

Insurers often cite a Federal Trade Commission study that draws a correlation between credit and risk that a driver will file a car insurance claim. Insurers that use credit-based insurance scores argue that the better your score, the lower the chances that you will file a claim, which typically means you’ll get better car insurance rates for having good credit.

Do any auto insurance companies not look at credit?

Unless an insurer specifically says it doesn’t use credit-based insurance scores as a pricing factor, it’s best to assume they all do if your state permits this practice. There are only four states—California, Hawaii, Massachusetts and Michigan—that ban the use of credit scores to help determine car insurance costs.

Some other states limit how insurance companies can use credit scores.

For example, Maryland prohibits car insurance companies from using credit history to determine if they will insure you, renew your policy, increase your costs or cancel your policy. But the laws in Maryland allow a credit review when you first apply for a policy, which helps determine what you’ll pay at your policy’s inception.

Some state laws require car insurance companies to disclose that your credit report can be reviewed and notify you if it results in an adverse action, such as higher costs.

How Credit Score Affects Car Insurance Rates

Drivers with poor credit saw an average rate increase of 79%, according to a Forbes Advisor analysis of rate increases and poor credit. That translates into an increase of over $1,560 annually on average.

Some states have done studies to examine how much of an impact the use of credit scores affects car insurance costs and found that most drivers end up paying less for car insurance.

For example, two-thirds (66%) of policyholders had lower car insurance costs with credit scoring in pricing, according to a 2016 study by the Vermont Department of Financial Regulation. Only 16% saw higher rates, and 18% saw no difference. A similar study by the Arkansas insurance department found that more than half (57%) of policyholders saw a decrease in car insurance costs, 23% saw an increase in costs, and 19% saw no change.

What Is No Credit Check Insurance?

Most car insurance companies use credit as a factor in setting rates—sometimes a very significant factor. Some insurance companies sell no credit check car insurance, meaning they will not use your credit-based insurance score as a factor to determine your car insurance rates.

But that doesn’t necessarily mean they’ll have the cheapest prices. It still makes sense to get car insurance quotes from multiple insurance companies before you buy a policy.

The use of credit as a pricing factor for car insurance is prohibited in California, Hawaii, Massachusetts and Michigan. There is no credit check when you apply for car insurance if you live in one of these states.

In other states, work with an independent auto insurance agent who can help you identify the cheapest car insurance options.

How to Save on Car Insurance if You Have Bad Credit

Poor credit is likely to affect your car insurance costs in states where the practice is allowed, but you have some options to save. Here’s how to find cheap car insurance.

Comparison shop

Not all insurance companies use credit as a price factor the same, so if you have poor credit, it’s crucial to compare car insurance quotes from multiple insurers. You can get free car insurance quotes:

- Online. Most car insurance companies offer free quotes online. You can visit several company websites and compare quotes. Or you can save time by using a website that provides quotes from multiple insurance companies at once.

- By phone or in person. You can call or visit a local insurance agent to help you find affordable car insurance options. An “independent” agent can sell policies from multiple insurers, while a “captive” agent only works for one insurance company and can only get you a quote from that insurer.

Check for discounts

Here are several common car insurance discounts to look for:

- Alumni, occupational and professional discounts. Some insurers offer discounts to members of alumni associations, fraternities, sororities, professional associations (like a union or bar association) and occupations (like educators).

- Anti-theft discounts. If your car has anti-theft features, you could find discounts ranging between 5% to 25% off your comprehensive car insurance coverage.

- Defensive driver discounts. Some insurers will give you a discount if you take an approved defensive driving course. Defensive driver discounts can range between 5% to 10%.

- Good driver discounts. Most car insurance companies offer discounts to drivers who steer clear of traffic violations and at-fault accidents. Good driver discounts can range between 10% to 40%.

- Good student discounts. If you have a student driver enrolled full-time at a high school or college, you could get a discount if they meet certain requirements, such as maintaining at least a B average. Good student discounts can range between 8% to 25%.

- Multi-car discounts. You can often find discounts ranging from 8% to 25% if you insure more than one car with the same company.

- Multi-policy discounts. If you buy other types of policies from the same insurance company—such as a homeowners insurance policy—you can typically score a discount between 5% to 25%. This is also known as a multi-line discount or commonly referred to as “bundling.”

- Usage-based insurance (UBI). You can often land an instant discount between 5% to 10% if you participate in your insurance company’s usage-based insurance program. UBI tracks and scores your driving habits. If you earn a good score, you could ultimately get a discount between 5% to 40%.

- Vehicle safety discounts. Car safety equipment like anti-lock brakes, airbags and daytime running lights can usually get you a discount.

- Other types of discounts. You can often get discounts for paying your car insurance policy in full, going paperless and paying by electronic funds transfer.

Avoid accidents and traffic violations

If a safe driving discount isn’t enough incentive, consider how much your car insurance costs will go up if you cause an accident or get nailed for a traffic violation (such as speeding). Here’s a look at how these types of incidents can negatively affect your rates:

- Car accidents. The national average rate increase after an accident is 38% for accidents that cause property damage and 40% for accidents that result in injuries.

- DUI or DWI. The national average rate increase after a DUI is 72%.

- Reckless driving. The national average rate increase for reckless driving is 61%.

- Speeding. The national average rate increase after a speeding ticket is 21%.

Choose the right coverage

How much car insurance coverage you choose is going to have a major impact on how much your car insurance costs. In most states, you’ll at least have to carry a minimum amount of liability car insurance. But the minimum requirements are usually inadequate, and it won’t provide coverage for your own car repair bills.

You’ll want to buy enough coverage to fit your specific car insurance needs without overpaying for coverage you don’t need. For example, you wouldn’t want to pay extra for roadside assistance insurance if you already have roadside assistance through another source, such as an automobile club.

Here’s a guide to help you determine how much car insurance you need.

How to Improve Your Credit Score

If you live in a state that allows car insurance companies to use credit scores as a pricing factor, you can help lower your car insurance costs by improving your credit score. Here are some tips to improve your credit score:

- Pay your bills on time. Late and missed payments are the biggest factors that affect your credit score.

- Lower your credit utilization. The amount of your credit limit you use affects your score. For example, if you have a $10,000 credit limit and debt of $7,500, you’re utilizing 75% of your available credit. Aim for 30% or less overall on individual credit cards.

- Check your credit report. You can get free credit reports from each of the three credit bureaus once a year at annualcreditreport.com. Reviewing your credit on an annual basis can help you spot any errors and take steps to correct them.

- Consider a secured card. A secured card is a credit card backed by a security deposit. You’ll deposit money into a bank account and will not have access to it while you have the card. Your credit card limit will be equal to the amount of your deposit.

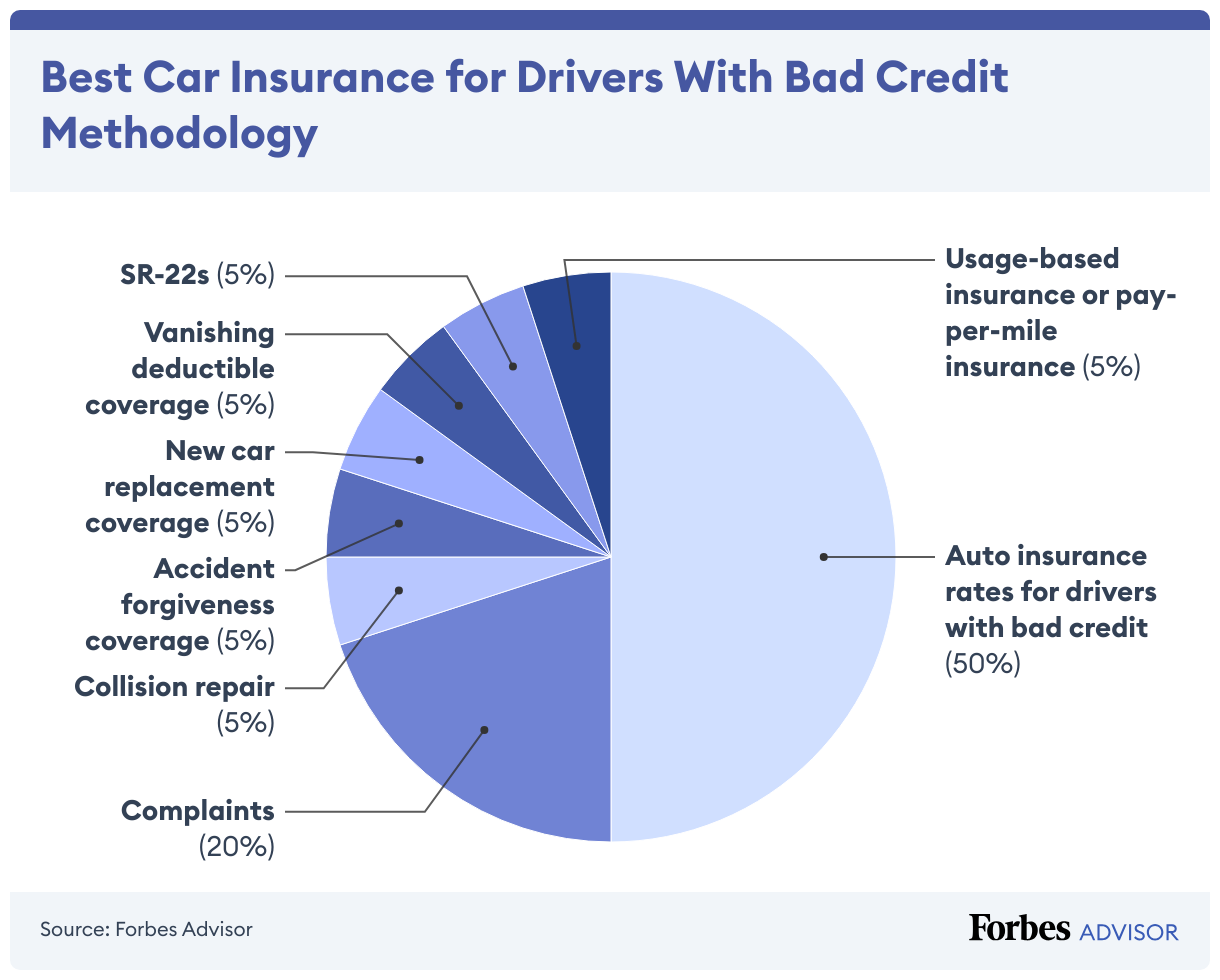

Methodology

To identify the best car insurance companies for drivers with bad credit, we evaluated each company on its auto insurance rates, the coverage options offered, complaints against the company and its collision repair process.

Auto insurance rates: 50% of score. We used data from Quadrant Information Services to find average rates from each company for drivers with poor credit.

Complaints: 20% of score. We used complaint data from the National Association of Insurance Commissioners. Each state’s department of insurance is in charge of logging and monitoring complaints against the companies that operate in their states. Most auto insurance complaints are about claims, including unsatisfactory settlements, delays and denials.

Accident forgiveness: 5% of score. Companies received points if they offer accident forgiveness.

New car replacement: 5% of score. Companies received points if they offer new car replacement.

Vanishing deductible: 5% of score. Insurers received points for having a vanishing deductible feature.

SR-22s: 5% of score. Insurers received points for providing SR-22s, which are required in some states for drivers with certain issues on their driving records, such as insurance lapses.

Usage-based insurance or pay-per-mile insurance: 5% of score. Companies received points if they offered one of these programs.

Collision repair: 5% of score. Auto body shop professionals have an insider view of each company’s approach to repairs. The better insurers don’t apply pressure to cut costs or install lower-quality repair parts. Some insurers also have processes that help speed up repair and claims processes, making for more happy customers. We used data provided by CRASH Network, a weekly newsletter covering the collision repair and auto insurance market segments. CRASH Network’s Insurer Report Card used grades from more than 1,000 collision repair professionals to gauge auto insurers on the quality of their collision claims service.

Car Insurance for Drivers With Bad Credit FAQ

Does applying for car insurance hurt my credit score?

No, applying for car insurance does not hurt your credit score. When insurance companies check your credit, they’re doing what’s called a “soft pull” that does not affect your credit score. That’s different from a “hard pull,” such as when you apply for a credit card.

It also doesn’t hurt your credit score to gather car insurance quotes from multiple insurance companies.

Will my car insurance go down if my credit score goes up?

While car insurance companies don’t use a typical credit score to determine your car insurance costs, improving your credit score can positively impact your credit-based insurance score, which can lead to better rates.

Here’s more about auto insurance scores and how it affects your car insurance costs.

Can you be denied car insurance due to credit history?

Yes, a car insurance company could deny your car insurance application due to poor credit, depending on your state.

Some states require the insurance company to tell you if they take an “adverse action” because of your credit history. Adverse actions include denying coverage, canceling coverage, not giving you the best rate or not giving you discounts. Your insurer should tell you the national credit bureau that supplied the information.

The use of credit for determining car insurance rates is banned in California, Hawaii, Massachusetts and Michigan.

What is a good credit score for car insurance?

What’s considered a “good” credit score at one car insurance company will vary from the next. That’s because insurers use credit-based insurance scores differently when setting their rates. And credit is just one factor insurers look at (in states where this practice is allowed). Your driving history, where you live, the type of car you drive and other factors will also play a role in your car insurance costs.

The key to finding the best car insurance is to shop around and get quotes from multiple insurance companies. Even if you have “good” credit, you’ll benefit by comparing quotes and finding the best prices.