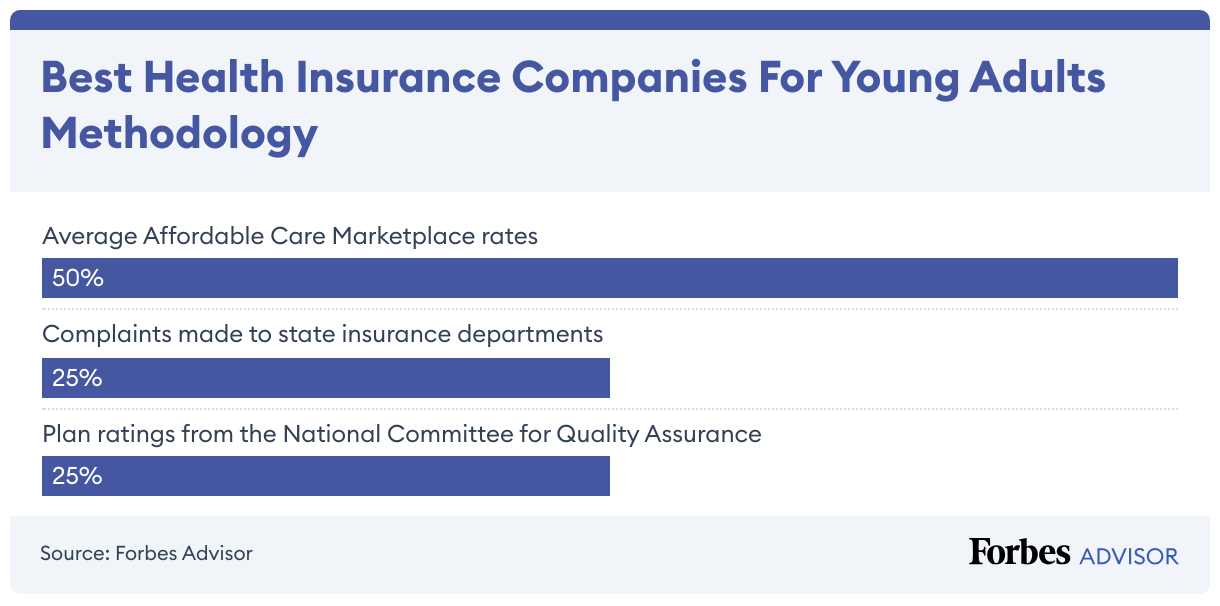

Shopping for health insurance requires comparing health insurance premiums and out-of-pocket costs, provider networks and types of plans.

Figure out your health plan eligibility

Your first step is to see the ways you can get health insurance. Maybe you can stay on your parents’ plan but also have access to coverage through an employer. Or perhaps you can get an Affordable Care Act (ACA) plan.

Once you figure out your insurance plan eligibility, you can move to the next step of deciding on a health plan’s benefit design.

Decide on benefit design

Health insurance plans have different names associated with benefit designs, including preferred provider organization (PPO), health maintenance organization (HMO), exclusive provider organization (EPO) and point of service (POS ) plans.

A plan’s benefit design can vary by whether you can get out-of-network care and if you need referrals to see specialists. The more flexibility and fewer restrictions you have in your plan, the more you pay for health insurance. That means PPOs usually cost the most and HMOs and EPOs are the cheapest plans.

Decide how much freedom you want in your plan, and then it’s time to compare costs.

Weigh premiums and out-of-pocket costs

Health insurance premiums are what you pay to have health coverage. These are a key piece of health insurance costs, but don’t forget about out-of-pocket costs like deductibles and coinsurance. These out-of-pocket costs come into play when you need health care.

See how much you would pay in premiums and compare those costs with out-of-pocket costs. For instance, if you’re comparing plans and one has a low premium with a high deductible, but the other has a higher premium and lower deductible, you need to figure out if you would rather pay more for coverage and less when you need health care or vice versa.

If you’re buying a health plan on the ACA marketplace, Bronze and Silver plans have the cheapest premiums but higher deductibles and out-of-pocket costs than Gold and Platinum plans. Gold and Platinum plans have higher premiums with lower deductibles. A Bronze or Silver plan could be a wise choice if you’re a young adult in good health and don’t expect to need much health care over the next year.

Check provider network

Health insurance companies contract with health care providers to create networks. These provider networks ultimately influence where you can get care and how much you pay.

If you have an HMO or EPO, you will likely have to stay within the provider network to get help from the health insurance plan. A PPO and POS generally allow you to get out-of-network care, but that comes at a higher cost.

Make sure the plan has a wide provider network in your area and your provider is on that network. You may otherwise have to pay all or most of the costs for out-of-network care.

Once you complete each step, you can choose between plans to find the right health insurance plan for you.